Russia will remain defiant against US sanctions pressure, Putin claims

4 hours ago

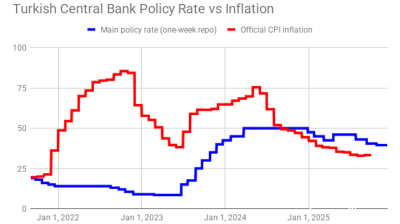

“Citizens of Turkey, this is your captain speaking: Prepare for a hard landing.” The Turks certainly won’t be hearing such a message from their president, Recep Tayyip Erdogan, in the run-up to the June 24 snap elections, but the opposition will be going all out to warn voters that the June 11 announcement of 7.4% in first-quarter GDP growth is a deceptive pre-poll gift as it merely demonstrates that their country’s overheating economy is set to come down to earth with a bump—something that should be demonstrated once the second-quarter figures are compiled.

“Above expectations, but at this stage pretty meaningless, as this was before re-balancing (weaker currency, higher rates, lower growth), which surely now will be the story for the second half, the only question is how much/how painful,” Timothy Ash, a strategist at Bluebay Asset Management, said in an e-mailed response to the latest GDP data.

"Crucially, this [GDP growth period] predates the recent financial market turmoil [in Turkey]," Jason Tuvey, an analyst at Capital Economics, said in a note to clients. "An abrupt slowdown is on the cards over the coming quarters."

The Q1 growth figure beat most market expectations, with a Bloomberg survey showing that markets expected 7%. Both China and India were left trailing Turkey last year as 2017 growth came in at 7.4% and Q4 brought 7.3%. Analysts talked of a “warp-speed” credit-fuelled expansion assisted with government stimuli and when Erdogan brought forward the parliamentary and presidential elections from November 2019 the opposition accused him of trying to hold on to votes he knows he might well lose when Turkey’s economic predicament dawns on the population at large.

Market reaction to the figures announced by statistics institute TUIK was negative but it should also be noted that the political uncertainty generated by the upcoming elections along with negative ramifications for Turkey of the present global economic and geopolitical environments—including rising yields on US treasuries—are a big part of what is weighing on Turkey’s emerging economy, highly dependent, as it is, on hot inflows of foreign capital.

The embattled Turkish lira (TRY) lost 1.31% d/d against the USD to trade at 4.5272 as of 13:00 local time while the benchmark Istanbul stock exchange index, the BIST-100, continued its nosedive, falling 1.92% to 94,033, the lowest level recorded since May 2017. On June 1, Fitch Ratings placed 25 Turkish banks and their subsidiaries’ Long-Term Foreign-Currency (FC) Issuer Default Ratings (IDRs) and Viability Ratings (VRs) on Rating Watch Negative (RWN), citing anxieties about the rising cost of their foreign currency funding, given the descent of the currency.

Foot off the brake

Erdogan is a self-described "enemy of interest rates" and he has regularly demanded cheaper money to spur more credit growth and construction, perhaps especially with an eye on the elections. His demands have come despite a spate of warnings from economic experts that Turkey needs to hit the brake. The central bank has been slow in its efforts to get ahead of the monetary curve and the markets fear that that is because Erdogan has been having the ultimate say over what the rate-setters are permitted to do. The worst-case scenario envisaged by some expert commentators is that Turkey’s currency collapse and surging current account deficit could spark a classic emerging markets currency-and-debt crisis.

In the latest growth figures, private consumption was gain the main engine with households’ final consumption in Q1 rising by 11% y/y, higher than the 6.6% seen in Q4 2017.

Consumer sentiment in Turkey declined by 2.8% m/m to 69.9 on the index in May, the lowest level recorded since December, data from TUIK showed on May 23.

On the production side, the construction industry grew 6.9%, higher than the 5.8% in Q4 2017, while industrial production grew 8.8%, showing no real change of pace.

Turkey’s Manufacturing Purchasing Managers' Index (PMI) dropped further into the red falling from 48.9 in April to 46.4 in May—its lowest level since April 2009, IHS Markit said on June 1.

Further economic warning signs can be seen in the industrial production numbers. Turkey’s calendar-adjusted industrial production index gained 7.6% y/y in March, slowing for the third consecutive month, data from national statistics office TUIK showed on May 16. A 13.7% y/y rise was posted in December and the annual growth rate has been declining since then.

Home sales declined by 8% y/y to 406,964 units in January-April while mortgage sales fell by 30% y/y to 117,292 units, TUIK reported on May 18.

Last week, the World Bank revised its GDP growth forecast for the Turkish economy in 2018 upwards to 4.5% from the previous 3.5%.