_0_1784176486.png)

Ukraine turns to police veteran as new Defence Minister to tackle mobilisation challenge

20 hours ago

Executive summary

Officials are working on taking Uzbekistan’s “opening up” policy, initiated by President Shavkat Mirziyoyev in late 2016, to the next level.

Mirziyoyev won a fresh mandate in the October 2021 presidential election, securing a landslide victory. With the country hoping a complete recovery from the effects of the coronavirus pandemic is now on the horizon, the Mirziyoyev administration knows there will be no time to waste in delivering gains delayed by the COVID-19 crisis.

However, events in Kazakhstan at the start of the new year may give officials pause for thought. The unrest seen across the neighbouring country might cause Tashkent to take stock of just how fast, and in what fashion, it can proceed in delivering more democratic and economic rights.

Uzbekistan will keep a wary eye on Afghanistan, while maintaining friendly relations with the country’s new Taliban regime in the hope that its neighbour can achieve enough stability to become a crucial element of Tashkent’s ambitions to expand trade with countries across South Asia. An Afghanistan slipping into an economic and humanitarian catastrophe would be somewhat alarming for the Uzbeks, especially from the security point of view. Tashkent has made several carefully elaborated calls to the West to do more to help the Afghans find their way to a sustainable future.

As the economy regains firepower, with the worst of the coronavirus crisis over, the international financial institutions are predicting growth of around 5.5% to 6% this year.

To improve the balance of payments equation, Tashkent is investing in adding value to production. Uzbekistan’s biggest export item is now textiles. The state is aggressively targeting value-added exports. Raw cotton exports have been banned. Cotton growers are thus forced to invest in textile production.

The introduction of inflation targeting is the main focus of the Central Bank of Uzbekistan (CBU). It is striving to anchor the population’s expectations for price rises, a tough task given the horrible experience with inflation Uzbeks had prior to the Mirziyoyev administration.

Every economic transformation needs funding, it goes without saying, but dabbing the brake, Tashkent has limited the total volume of domestic and foreign debt to 60% of GDP.

The banks continue to address their “neverending” lack of liquidity and rather high non-performing loan (NPL) ratios. In August, the LDR (Loan-to-Risk Ratio) for the entire Uzbek banking system hit a record 234%.

Uzbekistan’s commercial banks are expected to release $467mn in eurobonds by the end of 2022.

In energy, there are multiple major renewables projects. The government wants the share of renewable energy in energy generation to hit 25% by 2030. In nuclear, this year might bring the start of construction of the country’s first two plants, with the participation of Russia's Rosatom.

Retail players, meanwhile, say the supermarket sector in particular is “ready to boom”.

As 2022 unfurls, Uzbekistan, standing on the threshold of rich opportunity, will hope global economic winds don’t blow it off course.

Politics

In geopolitics, the re-elected Mirziyoyev is not expected to move far from the strategy long pursued by his predecessor, the late Islam Karimov, namely “taking the middle road”, rather than siding with major powers in key affairs.

Tashkent is cautiously strengthening relations with the European Union. Uzbekistan and the EU in the coming year will hold events including a meeting of the Uzbekistan-EU Parliamentary Cooperation Committee, the European Union-Central Asia ministerial meeting and an EU-Central Asia tourism forum.

Mirziyoyev’s first official trip after his election victory was to Russia. Vladimir Putin remarked: “Uzbekistan is not just our close neighbour, it is also an ally—this is exactly how we treat Uzbekistan. It is a large regional country with which we are connected in many ways—both historically and today.”

Much of the political situation in Uzbekistan will very much depend on how events further unfold in Afghanistan. The social unrest seen across Kazakhstan at the start of the new year might also give officials pause for thought as to how quickly, and in what fashion, more democratic and economic rights can be delivered.

Uzbekistan’s relations with the Taliban have been assessed by political analysts as friendly, evidenced by a number of bilateral negotiations between official figures.

The Taliban leadership promised “not to shoot a single bullet” towards its neighbour. Tashkent is proving helpful in the Taliban’s appeal for the unlocking of Afghan capital frozen abroad to help ward off an economic and humanitarian crisis, though Tashkent’s voice is only one of many in these matters. Uzbekistan clearly doesn’t want to see Afghanistan, on its doorstep, sliding into catastrophe and chaos. And a stable Afghanistan is vital to Uzbekistan’s hopes to build up trade and investment with South Asia.

One political event scheduled to take place in Uzbekistan in the coming year is a summit of the Organisation of Turkic States. The country will also host the regular meeting of the military department heads of the Shanghai Cooperation Organization (SCO) states.

Macro economy

Uzbekistan’s macroeconomic development in 2022 should be founded on gradual improvements in external and internal indicators, as long as no significant external risks come to pass. The US Federal Reserves battle with inflation could potentially have negative ramifications for emerging economies worldwide should it not go well.

If the pandemic is successfully beaten back, long-term restrictions on the migration of human resources and cross-border movement will not be introduced.

Key economic figures and forecasts

|

2016 |

2017 |

2018 |

2019 |

2020 |

2021

|

2022 .(forecast) |

|

|

Real GDP (% yoy) |

7.8 |

5.3 |

5.1 |

5.7 |

1.7 |

7 |

6 |

|

Inflation (% yoy) |

5.7 |

14.4 |

14.3 |

15.2 |

11.1 |

10 |

9 |

|

Unemployment rate (avg, %) |

5.2 |

5.8 |

9.3 |

9 |

10.5 |

9.8 (by 2Q) | |

|

Foreign trade balance (USD bn) |

20.1 |

22.4 |

28.2 |

41.8 |

32.1 |

37.9 (Jan-Nov) | |

|

Foreign direct investment (USD bn) |

1.7 |

1.8 |

0.69 |

6.51 |

6.6 |

7.6 |

|

|

Public debt (% of GDP) |

9.5 |

19.5 |

29.2 |

30.8 |

40.4 |

41.5 |

44.9 |

|

Source: Official statistics/World Bank |

|||||||

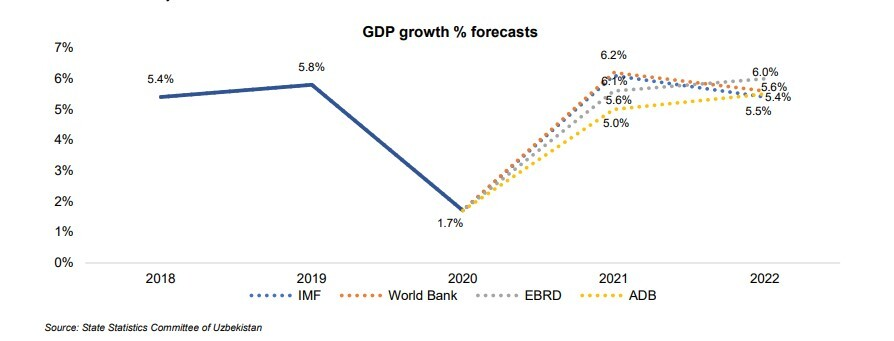

Before the pandemic hit, Uzbekistan’s GDP was rising at a rate of more than 6% a year. But in 2020 growth fell to a mere 1.7%. The bounceback in 2021 brought 6.9% in the first nine months, according to the Central Bank of Uzbekistan (CBU).

As the economy returns to health, the international financial institutions (IFIs) have upped their forecasts for 2022. The International Monetary Fund (IMF) revised its GDP growth outlook for 2022 to 6%. The World Bank is predicting 5.6%, while the Asian Development Bank (ADB) is a little more cautious at 5.5%. The highest growth rate is projected by the European Bank for Reconstruction and Development (EBRD). It sees 6%.

External environment

Uzbekistan’s foreign trade has expanded significantly since incumbent Shavkat Mirziyoyev took office in 2016. Since the liberation of the FX market in 2017, companies have leapt at the chance to seal their own export deals and trade is flourishing.

According to official data for January-October 2021, Uzbekistan’s foreign trade turnover got back on the rails following the impacts of the first year of the pandemic, reaching $32.7bn, up 8.5% y/y.

Of the total trade volume, exports amounted to $12.4bn, (down 6.7%), while imports surged 20.5% to reach $20.2bn.

Among the 20 major partner countries of Uzbekistan in foreign economic activity, active foreign trade balances were observed with four countries—Afghanistan, Kyrgyzstan, Tajikistan and Turkey.

China remains Uzbekistan’s most important trade partner. However, turnover with the “ancient” counterpart did not in 2021 regain pre-pandemic levels, whereas trade with the other Central Asian republics and Turkey did surpass the levels seen in 2019.

To improve the balance of payments equation, Tashkent is investing in adding value to production. Uzbekistan’s biggest export item is now textiles. That in itself is a reflection of the state’s new policy of aggressively targeting value-added exports. A ban on raw cotton exports has forced cotton growers to invest in textile production.

Accessions into the EU Generalised System of Preferences Plus (GSP+) scheme and its UK analogue (Generalised System of Preferences Enhanced Framework) will yield trade gains in coming years as tariffs are slashed.

If the country finalises its decision to join the World Trade Organisation (WTO), foreign trade figures can be expected to skyrocket.

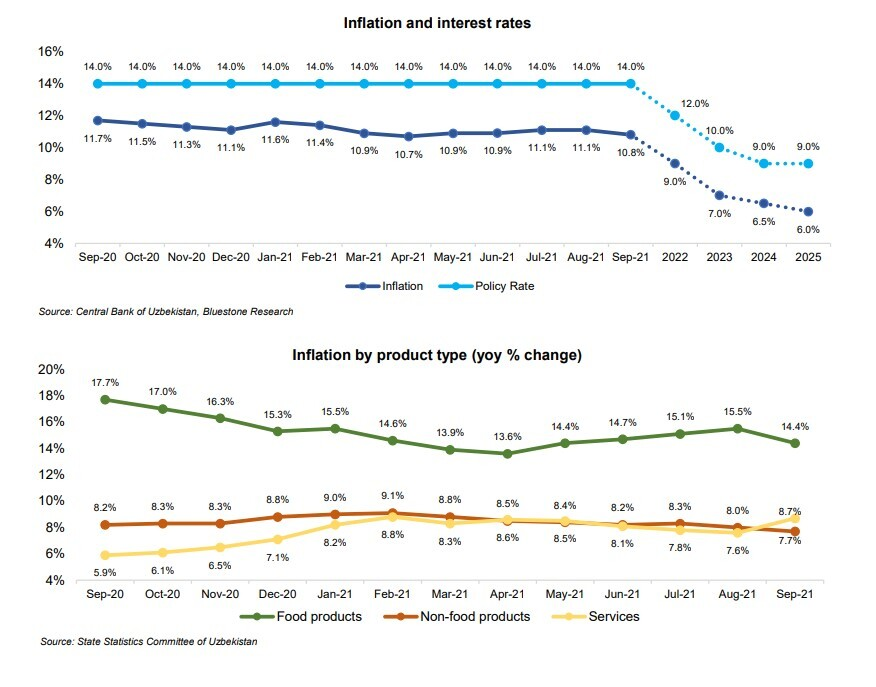

The government forecasts that inflation will decline to 10% by the end of 2021, 9% in 2022 and 5% in 2023.

European Bank for Reconstruction and Development (EBRD) economist Eric Livny observed to bne IntelliNews that even 10% was a rather high figure, but such price growth was not an Uzbek phenomenon as, amid the pandemic, inflation had gained momentum worldwide.

“Inflation in Uzbekistan is slightly lower this year than in previous years. There is a long-term downward trend, which is very good. But in general, it still remains high. This is a serious headache for the population. Especially if we are talking about food, basic necessities. People who live on a pension or on a single salary, or even three salaries, they are forced to work from morning to evening. For them, inflation is a very serious blow to their pocket,” said Livny.

The introduction of inflation targeting is now the main focus of the Central Bank of Uzbekistan (CBU), which has been trying to anchor the population’s expectations for price rises.

After the centralised controls on the economy were eased in the first quarter of 2020, inflation fell. It declined from a steady 15.5% to reach a low of 7.3% in October 2021. That allowed the CBU to make a series of rate cuts.

Nevertheless, the basic problem the central bank faces is that having lived through decades of economic chaos, the population has little confidence in the regulator, thus the inflation expectations of the population and businesses have never been anchored. Expectations for price rises remain significantly higher than those seen in CBU forecasts, which is in itself inflationary.

Debt

In 2020, the government limited the sourcing of external loans on behalf of the government or under its guarantee. It also limited the total volume of domestic and foreign debt to 60% of GDP.

According to Ministry of Finance data, the public debt is projected to reach $33.5bn, or 44.9% of GDP, in 2022.

The state's external debt is forecast to amount to $30.4bn (40.7% of GDP). A total of $23.5bn is to be raised on behalf of the government, while $7.5bn is be taken under state guarantee.

The growth in the public debt is associated with the sourcing of additional external borrowings. These funds will primarily be channelled towards financing responses to the consequences of the COVID-19 pandemic and supporting the economy and the population.

According to the World Bank’s Autumn 2021 Europe and Central Asia Economic Update, the government debt of Uzbekistan is set to amount to 42.5% of GDP in 2022 and 42.2% in 2023.

The Uzbek retail market is becoming increasingly attractive. The supermarket sector in particular has been singled out as “ready to boom”. The introduction of organised retail has led to rapid development.

Finance minister Timur Ishmetov noted that there were rapid advances because retail in Uzbekistan is one of the few sectors with no state presence. The government doesn’t own stores and restaurants. They can move ahead fast.

The country’s total annual retail market volume is estimated at between $6bn and $8bn, of which supermarkets —or “organised retail”— make up between just 7% and 10%. This share, according to experts, is set to at least triple to 30% in the next five years. Retail turnover reached Uzbekistani som (UZS) 167,026bn ($15.6bn) in the first nine months of this year, according to investment bank Bluestone, up 9.8% y/y. By November, annual growth stood at 10.5%.

The European Bank for Reconstruction and Development (EBRD) has invested $40mn to take a stake in Korzinka, one of the biggest supermarket chains in Uzbekistan, while giant French grocer Carrefour became the first international retailer to enter the Uzbek market last year, intending to invest $100m.

Korzinka, which accounts for half of all supermarket turnover in the country, anticipates expanding its chain from 68 to 150 stores by 2025. Carrefour has opened three stores and has plans to open six more by year-end. The biggest expansion is expected from Makro, Uzbekistan’s current leader by number of stores, with 109 stores, mainly supermarkets and express outlets. Makro plans to have between 800 and 1,000 stores in Uzbekistan in the next five years, according to its chief executive, Roman Sayfulin.

The latest addition to the increasingly hot Uzbek retail sector, Ukraine and Moldova's largest online retailer Rozetka, has arrived on the Uzbek market. It launched website rozetka.uz in September. The site offers household appliances, electronics, sports equipment, books, children's toys and more. After just two months of commissioning, in November it announced an expansion of delivery points in the Uzbek capital. Vladislav Chechetkin, co-founder of the online store, said that two delivery points were already operating in Tashkent, and there were plans to open four more.

Uzbek banks experienced both positive and negative news in 2021.

Let's start with the bad. The biggest headache for domestic banks was their “neverending” lack of liquidity and rather high NPL (non-performing loan) ratios. In August, the LDR (Loan-to-Risk Ratio) for the entire Uzbek banking system hit a record 234%. For banks with a state share, it was even higher at 301%, twice as high as seen in the US, three times higher than the global average and 3.3 times higher than the average for developing countries.

As of January 1, the share of NPLs stood at 2.1%, but by August 1 it had grown to 6.2%. The amount of loans provided to the Uzbek population, meanwhile, over the past three years has increased 3.3-fold. The banks were not ready to account for NPLs in such volumes. But by November 1, the NPL ratio declined to 5.7%. It is set to normalise in the coming months.

Turning to the good news. One of the most positive changes the banking sector has started to witness is privatisation. A massive privatisation campaign is in it its infancy by now. It is expected to yield results in the coming years.

The banking system of Uzbekistan is characterised by high concentrations: 84% of all bank assets are still owned by state-owned banks, and 64% belong to five of the biggest state-owned banks (National Bank, Asaka Bank, Uzpromstroybank, Ipoteka Bank and Agrobank).

The privatisation of Uzpromstroybank and Ipoteka is set to be completed by the end of 2022. Both financial institutions were included in the most profitable bank top three rankings following the release of the 3Q results. Further plans include the privatisation of Asaka Bank, Aloqa Bank, Qishloq Qurilish Bank and Turonbank.

In January-October 2021, Uzbek enterprises produced industrial products worth UZS 356.1 trillion ($33.1bn), up 9.5% y/y.

The structure of industrial production was as follows:

manufacturing industry - 82.9 %

mining - 9.6%

provision of electricity, gas, steam and air conditioning - 6.8%

water supply, sewerage, waste collection and disposal - 0.7%.

The creation of special economic zones (SEZ), the number of which has increased from seven to 21 over the past five years, and small industrial zones (SIZ) (up from 63 to 77), technoparks and clusters, have become the main elements for the development of industrial production.

The government aims to ramp up the sector through the implementation of new projects, supporting low-power or idle enterprises and efficiently utilising empty buildings.

President Shavkat Mirziyoyev during his 2021 election campaign unveiled plans to expand the volume of industrial production by 1.4 times over the next five years.

The year of 2020 brought huge reforms in Uzbekistan’s power sector. Addressing world anxiety over climate change, the government unveiled planned contributions in addressing the issue.

In particular, by 2030, the government aims to cut greenhouse gas emissions by 35% compared to the levels recorded in 2010, as the climate in Central Asia is changing twice as fast as in other regions due to the drying up of the Aral Sea.

At the national level, Uzbekistan is implementing a comprehensive strategy for its transition to a green economy and a programme for the development of renewable and hydrogen energy. Some 200mn tree and shrub saplings are to be planted in the country annually.

By 2030, the energy efficiency of the economy is set to double, with the share of renewable energy comprising at least 25%.

Moreover, the year 2022 is set to see the construction of two nuclear power units with the participation of Russia's Rosatom, an initiative that has caused concern among Uzbeks and people in neighbouring Kazakhstan.

The biggest projects in the energy sector are currently under way with the participation of Total Eren (France), Masdar (UAE) and Aqua Power (Saudi Arabia).

Major lenders in the sector are EBRD and ADB.

Meanwhile, the volume of electricity generation at Uzbek hydroelectric power plants (HPPs) fell by almost 23% in 2021 amid low water levels.

Power generation at HPPs fell to 5bn kWh in 2021, against 6.5bn kWh in 2019.

Uzbekistan’s construction boom regained momentum in 9M2021. Growth of 4.5% y/y was posted compared to the 0.1% recorded by the sector in 1H 2021. Nevertheless, the figure is expected to decline in 2022, following an order announced in September by President Shavkat Mirziyoyev, who said: "Enough is enough. If we continue, the sewage system will not stand the strain, and neither will the people, and there will be no green territory, everything will turn into concrete."

The construction boom has also caused concern among the population, with the finger pointed at officials for elements of the climate crisis observed in the country.

A sudden and severe dust storm struck and engulfed Tashkent and several regions on the evening of November 4. Inhabitants claimed it resulted from “reforms” in the construction sector and a “massive tree cutting campaign” initiated following these “reforms”.

According to the national statistical committee, cement production at Uzbekistan’s largest producers reached around 8mn tonnes in the first eight months of 2021, marking an increase of 18.2% y/y, while cement prices rose by 2.4% in 9M 2021, in part due to a 550,000-tonne rise in cement imports.

Meanwhile, Central Asia's largest cement plant Qiziliqumsement has invested $112m to add a fourth production line.

The line will add 2.2mn tonnes/year of cement to output, bringing total output to 5.8mn tonnes/year, a bit less than a third of Uzbekistan’s entire cement production.

According to plans, some 50,000 apartments will be commissioned next year under mortgage programmes. Funds totalling $1.2bn will be allocated for this purpose.

Fiscal policyBudget revenues

State budget revenues in 2022 are projected to hit $18.58bn, or 23.8% of GDP (in 2021, $15.88bn, or 23.6% of GDP).

Value-added tax (VAT) is set to generate the lion’s share of revenue ($4.95bn); the profit tax share is to comprise $4bn.

Tax

According to the Ministry of Finance, the growth in state budget revenues will insignificantly affect the total tax burden.

The tax burden for 2021 was forecast at 23.6%; in 2022 this figure is expected to amount to 23.8%.

Direct taxes will be worth $6.3bn, amounting to 34.3% of total state budget revenues or 8.2% of GDP.

Indirect taxes will amount to $6.79bn (36.6% of total state budget revenues or 8.7% of GDP).

The state budget revenues in 2022 will very much depend on the economic situations of enterprises. The top 10 enterprises are set to provide around 36.4% of state budget revenues. The contributions would break down as follows:

NMMC — 17.82%;

AMMC — 9.4%;

Uztransgaz — 1.89%;

Uzbekneftegaz — 1.7%;

UzBAT — 1.5%;

Hududgaztaminot— - 1.26%;

Uz-Kor Gas Chemical — 0.78%;

Uzmetkombinat — 0.76%;

UzAuto Motors — 0.73%;

Bukhara Oil Refinery — 0.6%.

Budget expenditures

State budget expenditures in 2022 are forecast to amount to $19.9bn, or 25.6% of GDP (the forecast for 2021 was $17.7bn, or 26.4% of GDP). To stimulate economic growth, the government plans to increase the funds allocated towards the implementation of sectoral development programmes.

The social sphere and segment for the social protection of the population is to in 2022 account for $9.8bn, or 49.1%, of total state budget spending.

The largest share (44.5%) of social expenditures will be spent on education ($4.3bn).

The healthcare sector will account for $2.1bn.

Some $223mn will be allocated from the budget for the procurement of medicines and medical devices, vaccines and pharmaceuticals. Separately, $157.9mn will be provided for the implementation of measures against coronavirus (COVID-19) infection.

Cultural expenses will amount to $167.2mn.

Funds totaling $2.2bn will be channelled to support economic reforms.

Budget deficit

By the end of 2021, the consolidated budget deficit was projected to reach 5.5% of GDP.

In the medium term, a gradual reduction of the deficit is planned to ensure the sustainability of the public finances.

In 2022, the consolidated budget is forecast to have a deficit of $2.3bn (3% of GDP).

Starting from 2023, the government plans to introduce an operational budget rule that sets a limit on the size of the deficit of the consolidated budget at 3% of GDP.

High inflation observed in the country over the years has forced the central bank to keep its monetary policy rate relatively high.

However, banks with access to dollar funding have been able to afford the offering of significantly lower rates on dollar loans. The spread between the cost of borrowing in Uzbekistani som and dollars is so wide that most borrowing is done in FX. That exposes Uzbek companies to significant FX risks.

According to Mirsaid Nosirov, an analyst at the regulator, the dollar share of loans was 48% as of November, but there had been a gradual decline.

With retail deposits paying 17.5% and loans costing 21% in som, there was a 3-4% spread that remained a disincentive for business to borrow for investment capital in the local currency. However, Nosirov pointed out that the som has been very stable and only depreciated against the dollar by 2% in the first nine months of 2021.

The central bank has to be worried by the dollarisation of credits as other countries, such as Ukraine and Poland, have come-a-cropper in the past by exposing themselves to FX risks that proved too big.

The share of dollar loans has fallen from 70% previously to around 50%:50% local vs foreign exchange now.

“Things are changing now thanks to the stable currency and falling inflation,” said Nosirov. “But they will take several years to normalise.”

According to the AFC Uzbekistan Fund, 2021 was a transitional year on the road to significant capital markets catalysts that will be seen in 2022. Earnings growth for companies listed on the Tashkent Stock Exchange continued its strong performance last year.

AFC has also divided Uzbekistan’s capital market into three phases. It expects Phase II to occur between 2022-2025. This phase should see certain state-owned enterprises (SOEs), what it calls the “crown jewels” of Uzbekistan’s economy, being privatised through domestic IPOs and SPOs and eventual dual listings abroad, likely in London. These companies include the national airline, Uzbekistan Airways, one of the biggest gold mining companies in the world, Navoi Mining and Kombinat, a leading copper producer, Almalyk Mining and Metallurgical Kombinat, and one of the largest steel plants in Central Asia, Uzmetkombinat, among others. These listings should attract significant foreign and local capital to the Tashkent Stock Exchange, increasing liquidity and interest in the market.

"Phase III is expected to involve IPOs by private sector companies once the stock market is liquid and has enough investor participants, both institutional and retail, to absorb larger share issues. “This phase should overlap with Phase II and we are already seeing private sector companies expressing an interest in eventual IPOs, which is highly encouraging," Scott Osheroff, an AFC analyst, said.

Odilbek Isakov, a Deputy Finance Minister, earlier announced the government’s plans to hold 15 IPOs in the next three years, including IPOs of equity in five state-owned banks, three insurance companies and metallurgical and other companies.

Isakov added that new financial products were to be released, including ETFs for gold, mortgage bonds and sukuk.

The government is also planning to issue bonds linked to inflation, while the Uzbek and international depositories will be connected.

For Uzbekistan, 2021 can truly be named the “Year of Bonds”. Dozens of large issuers joined the “eurobond bonanza”, initiated by the government back in 2019.

Capital markets “reforms” are expected to continue in 2022.

Mining giant Almalyk Mining and Metallurgical Combine (AMMC) plans to issue $500mn of eurobonds during the first half of 2022.

A eurobond debut is anticipated from Asakabank. Fitch Ratings assigned the bank’s upcoming issue of UZS-denominated senior unsecured eurobonds an expected long-term rating of 'BB-(EXP)'.

President Shavkat Mirziyoyev during his pre-election campaign said that commercial banks would release $467mn in eurobonds by the end of 2022.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now