India's new diplomacy of trade deals

11 hours ago

Politics

After pro-EU candidate Maia Sandu defeated the pro-Russian incumbent Igor Dodon to take Moldova’s presidency in December 2020, her Party of Action and Solidarity (PAS) won a clear majority in the parliamentary elections of July 13, 2021. A government was quickly appointed, headed by Prime Minister Natalia Gavrilita.

Upon gaining majority support in parliament, President Sandu and her party announced thorough reforms in the judiciary, starting with external evaluation of judges and prosecutors. General prosecutor Alexandr Stoianoglo has been suspended and investigations were launched against him. But the process was hasty and created the impression of poor coordination and superficial legal justification of the actions, allowing the opposition to criticise the process.

Speaking of the opposition, Andrei Nastase’s Dignity and Truth Party (PPDA) has expressed moderate support and frequent criticism in regard to the new PAS government. Currently not holding any MP seat, the PPDA can be regarded as “the pro-EU opposition” to the government. The “pro-Russian opposition” is formed by Dodon’s Socialist Party, which joined forces with Vladimir Voronin’s Communist Party.

The electorate’s overwhelming pro-EU vote in the last two elections was followed by political and financial support for Moldova from EU institutions and individual countries, particularly from Romania. The European Commission and Romania resumed the assistance programmes suspended in the past for deviations from the path of reforms and extended financial support to Moldova to mitigate the effects of the COVID-19 pandemic. In November, the Commission extended a €60mn grant to help the country overcome the natural gas crisis created by Gazprom cutting the gas supplies by one third.

Moldova’s relationship with Russia is in the process of normalisation, after Dodon attempted to bring Moldova closer to the political and economic organisations controlled by Moscow, primarily the Eurasian Economic Community (EEC). The new government in Chisinau discontinued the country’s participation as an observing member to EEC meetings while concomitantly intensifying diplomatic ties with the European organisations, pinpointed by Sandu’s frequent visits to Brussels and other European countries. Foreign Minister Nicu Popescu visiting Moscow expressed cautious and moderate positions, seen by some as too moderate particularly in regard to the Russian troops in the Moldovan separatist republic of Transnistria.

Macroeconomy

GDP growth: The Moldovan economy grew by 10.3% y/y in the first three quarters of 2021, fully reversing the slowdown in 2020. Compared to the first three quarters of 2019 (before the crisis), Moldova’s economy expanded by 1.2%. It is a small advance, yet more than initially expected.

Most sectors of the economy performed well: agriculture generated 14% y/y more value added, construction +5.3% y/y, industry +9.8% y/y and IT & C +11.9% y/y.

Domestic demand still relies to a large extent on imports. Consumption (+11.5% y/y in January-September) and gross fixed capital formation (+7.9% y/y) taken together exceeded the country’s GDP by 28% in the three quarters.

Imports, expressed in comparable prices, rose by 23% y/y — more than three times faster than exports (+6.5% y/y).

For the whole year 2021, growth may end up exceeding the official 6% forecast and even the 6.8% forecast of the World Bank or the 7% projection sketched by the European Bank for Reconstruction and Development (EBRD).

For 2022, the government expects 4.5% growth, slightly more than the EBRD’s 4% forecast. The low base effects and the resumption of external financing support expectations for even stronger performance depending, however, on further waves of COVID-19 that may defer investment projects by foreign manufacturing groups that will likely seek to develop or relocate to Moldova new production facilities.

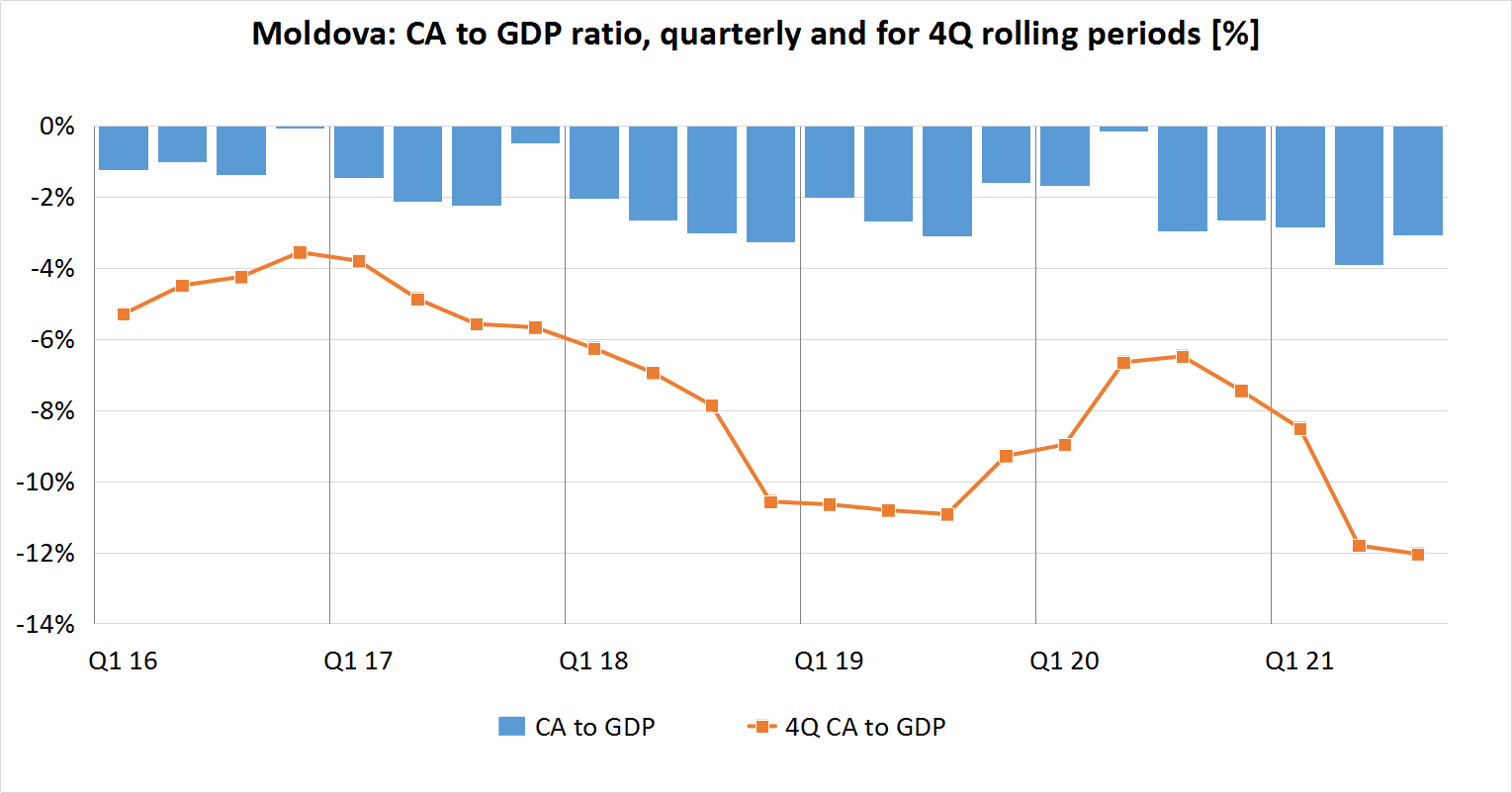

External environment: Moldova’s current account deficit widened by 14% y/y in the third quarter of 2021, to $400mn. The deficit in the four-quarter period ending September 2021 increased to $1.57bn, from $1.52bn calculated three months earlier. Compared to the four-quarter period ending September 2020, the current account (CA) gap doubled — but this is because the gap has narrowed during the lockdown period. Compared to 2019 (the last full year before COVID-19 crisis), Moldova’s CA gap still widened by 41%.

The country’s external deficit thus reached a new all-time record, both in absolute terms and compared to its GDP: the four-quarter CA gap accounted for 12% of the GDP over the same 12-month period ending September 2021.

The net import of goods, typically large in Moldova compared to GDP as a result of robust remittances financing private consumption, increased by 16% y/y to $1.07bn in Q3 and by 30% y/y to nearly $4bn in the rolling four-quarter period ending September. The net imports in the 12 months ending September thus accounted for 30% of GDP.

Wage remittances in the four-quarter period ending September (including transfers to households) remained below 14% of GDP but still financed 43% of the net import of goods. The remittances to GDP ratio has gradually declined from 16.4% in 2016 to 13.7% despite reaching a new record of $1.78bn in the four-quarter period ending September, up from $1.33bn in 2016.

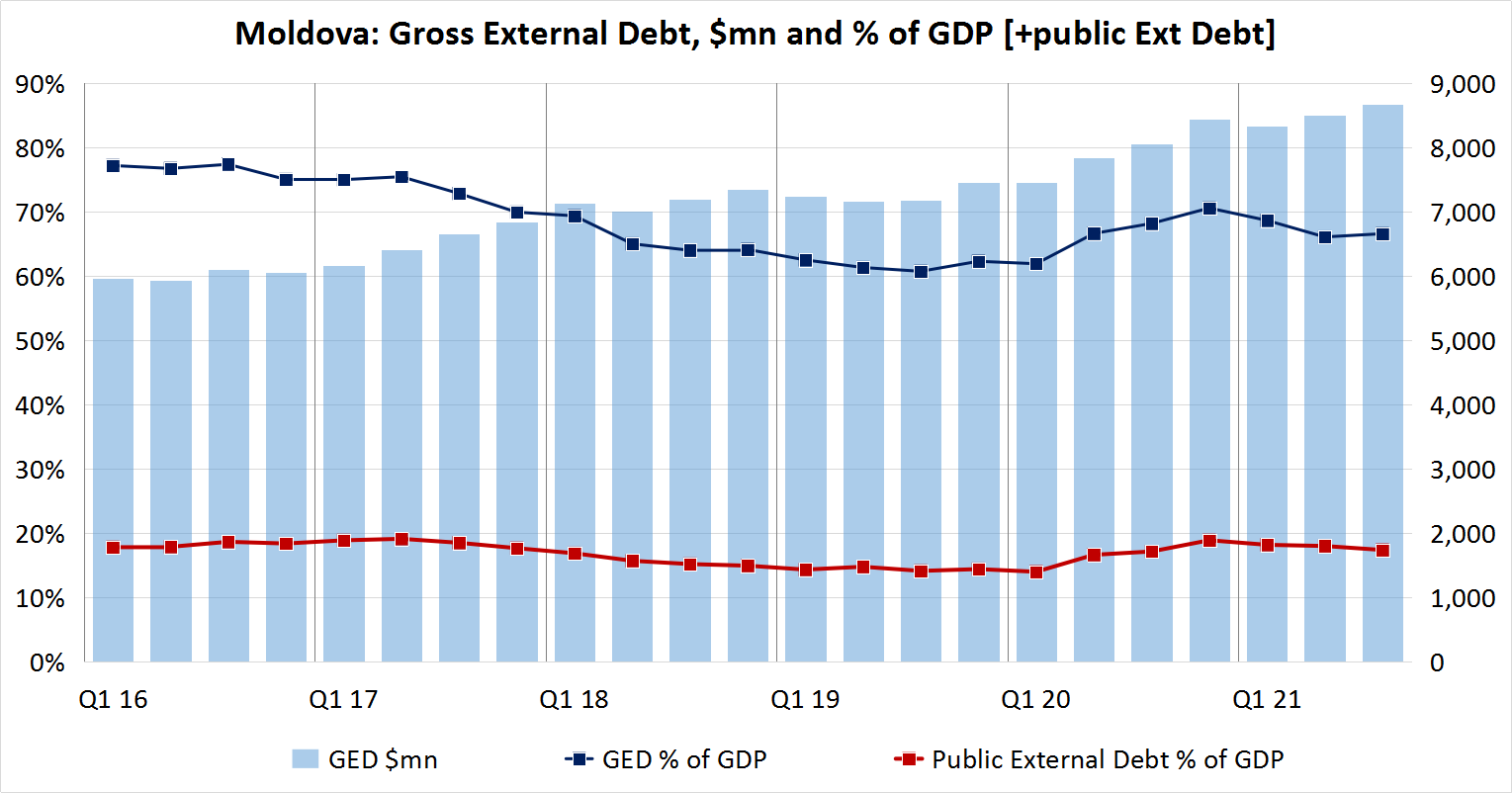

Moldova’s gross external debt (GED) increased by 7.5% y/y as of the end of September 2021, to $8.66bn — or 66.5% of the four-quarter GDP calculated at the same date. In absolute terms and as a share of GDP, the country's GED picked up in Q3. Robust financing from abroad will further push nominal GED up over the coming years, while the indebtedness ratio is likely to advance at more moderate levels as the nominal GDP keeps expanding.

Compared to the end of September 2019, Moldova’s GED surged by 20.7%, as the country received financial support from international financial institutions (IFIs) during the COVID-19 crisis and the non-financial corporations borrowed from abroad as well.

Thus, the government’s gross external debt ($2.26bn or 26% of total GED and 17.3% of GDP) increased by 35% compared to September 2019 and contributed $591mn to the overall $1.48bn rise in GED over the past two years. Non-financial corporations’ GED (over 40% of total GED) increased by 22% over the past two years, or by $623mn.

Inflation and monetary policy: Moldova’s headline inflation soared from 8.8% y/y in October to 12.4% y/y in November as the natural gas price soared by 80% as of November 1.

The National Bank of Moldova (BNM) decided to increase the refinancing rate by 1.0 pp to 6.50% at its December 3 meeting.

This was the fourth rate hike this year to address rising inflation and inflationary expectations. Further monetary policy tightening may follow, as the inflation was not the result of only temporary rise in the energy prices. In November, the BNM doubled the forecast for next year’s average inflation to 14% y/y.

Industrial production: Moldova’s industrial activity on average and in most of the sectors has recovered to pre-crisis levels already. In the 12-month period ending October 2021, the industrial output increased by 4.8% y/y and by 3.8% compared to 2019.

The food and beverage industries as well as the industries related to the automotive sector (electric and electronic equipment production) still lag behind pre-crisis period. Specifically, food production in the latest available 12-month period was 2.5% smaller than in 2019 and beverages production contracted by 6.5%. The production of electric and electronic devices contracted by 28% and 14% respectively. The production of construction materials, metal products and metal constructions boasted growth rates of over 20% compared to 2019. Light industry and wood processing also performed well. Furniture production, with a 78% leap (both y/y and compared to 2019), made the strongest advance.

Real economy

Retail: Foreign and local retailers are capitalising on the robust growth of private consumption.

Retail sales in Moldova, over the 12 months to October 2021, increased by 14.0% y/y and by 16.1% compared to 2019, the last full year before the crisis. It is an outstanding advance pinpointed by the expansion of the modern retail chains and the consolidation of local players.

The main foreign player, Kaufland, continued its expansion on the Moldovan market while the largest local retailer took over its rival, gaining more power.

In only two years, the German retailer opened six hypermarkets in Moldova, taking a head start in expanding its network well ahead of other foreign retailers. It has three stores in Chisinau and one each in Balti in the northern part of the country, Ungheni on the border with Romania and Comrat in the Gagauz administrative unit. Moldretail Group, the largest player in food retail in Moldova, controlled by local businessman Vasile Dragan and operating the Linella chain of stores, took control of rival group Fidesco in the largest transaction on this market recently.

Moldretail Group is the biggest retailer and the biggest company by turnover in Moldova, with revenues of MDL4.66bn (233mn) and a profit of MDL179mn in 2020. The group is best known for its Linella chain of stores, which has reached 120 units, including 55 in Chisinau, being the largest in food retail.

Founded in 1992, Fidesco Group is one of the first and largest retail supermarket chains in Moldova. Currently, the Fidesco group includes 35 stores in the capital city Chisinau and the countries’ biggest cities.

Banks: Moldovan banks, virtually untouched by last year’s crisis, boasted robust 2% return on assets (ROA) and 12% return on equity (ROE) in January-September 2021.

In the first three quarters of 2021, the profit of the banking system of Moldova amounted to MDL1.65bn (€82mn), increasing by 44.1% compared to the same period of 2020 and nearing the value recorded in the same period of 2019, MDL1.77bn.

Total assets amounted to MDL113.8bn, 9.6% more than at the end of 2020 (ytd). This resulted in a robust annualised ROA rate of 2.0% (0.5pp up from 2020) and annualised return on equity of 12%, 3.2pp up from 2020. Total revenues amounted to MDL6.4bn, 13.9% up y/y. Of this, interest income accounted for 56.6% and non-interest income 41.4%.

During the first nine months of 2021, the share of non-performing loans (substandard, doubtful and compromised) in the total portfolio of loans decreased by 0.6 pp, amounting to 6.8% at the end of September 2021. The indicator, however, ranges between wide limits, from 2.2% to 12.6%, depending on the bank. At the same time, the stock of non-performing loans in absolute value increased by 8.1% ytd to MDL3.6bn.

In January-September 2021, Moldovan banks continued to maintain liquidity indicators at a high level. Thus, the value of the long-term liquidity indicator, which is supposed to remain under 1, was 0.76, not changed from the end of 2020.

Moldova Agroindbank (MAIB), the biggest bank in Moldova with around 30% of the banking system’s total assets, aims to launch an IPO around 2023-24 in London, Amsterdam, Warsaw or Bucharest.

The bank is 41% controlled by the European Bank for Reconstruction and Development (EBRD) in partnership with two investment funds.

The bank is already listed on the Moldovan stock exchange, however, the local bourse lacks liquidity.

Fugitive businessman Veaceslav Platon, one of the bank’s former owners, has warned that the move would be risky as long as he still seeks to recover his shares in court.

Industry: Moldova’s stronger commitment to EU integration, affirmed by the newly elected authorities in Chisinau, is likely to result in more investments made by European industrial groups. Better contract enforcement and cutting the red tape — promised by the government — are needed to address investors’ concerns, while poor transport infrastructure remains a long-term problem.

Three Moldovan businessmen, Valentin Esanu, Andrei Zabolotny and Alexandru Rotaru, are planning to build a metallurgical plant with an annual capacity of 100,000-150,000 tonnes of steel upon an investment of $16mn. Production is planned to start in autumn 2022. Esanu will finance 35% of the investment through his company Solifarex Plus, which collects and exports scrap metal, while the rest of the money will be invested by his partners. The company also plans to take out bank loans.

At this moment, Solifarex Plus exports 9,000-10,000 tonnes of scrap metal per month to Turkey, out of which part will be used in the new steel plant rather than being exported. The new company aims to process the steel it produces from scrap metal, into rebar and sell it on the local market or export it to Romania. Around 5,000 tonnes of rebar will be exported in Romania each month, according to investors’ business plan.

The project developed by the three businessmen, who set up Omni Steel company for this purpose, was unveiled in early November when Prime Minister Natalia Gavrilita paid a visit to the free economic zone FEZ Balti, which is going to host the plant. Geographically, the plant will be located in Panasesti village, Straseni district, 30km north of Chisinau.

Austrian group Gebauer & Griller will build its third factory in Moldova, thus increasing its investment in the free economic zone (ZEL) Balti by another $14mn, the company announced. Construction of the factory, through Gebauer & Griller's Moldovan subsidiary GG Cables and Wires EE, is set to begin in November, and 500 new jobs will be created at the factory. The company also intends to invest another $51mn over the next three years, which would bring its total investments in Moldova to $72mn.

GG Cables and Wires EE was registered in Moldova in 2012 as part of Gebauer & Griller, based in Vienna. Currently, the company owns two production plants located in the Balti Free Economic Zone. The main activity of GG Cables and Wires EE in Moldova focuses on the production of insulated wires and cables.

Energy & power: After a brief gas crisis seemingly prompted by Moldova’s pro-EU ambitions that were firmly expressed by President Maia Sandu and her new government, the country sealed a relatively favourable five-year contract with Gazprom. This gives the country time to set in place a decently functioning retail market for electricity and ga) and prepare necessary infrastructure to increase competition on the wholesale market or at least find alternative suppliers. For this, the country needs massive investments in infrastructure and to set up a functioning market in order to prevent situations like the one in November 2021. This is hard to achieve as long as Inter RAO sells Moldova electricity produced in the separatist republic of Transnistria using natural gas that it receives from Gazprom but does not pay for. This political game has to be discontinued one way or another if the pro-EU regime in Chisinau sincerely seeks to set in place a functioning market.

But above all, Moldova needs to prepare to face high energy prices. This can be done by sharp appreciation of the local currency supported by a significant amount of foreign investments. This is the optimistic scenario.

Moldova is still fully dependent on Russian natural gas and the Russia-controlled power plant in separatist Transnistria. Changing this can be achieved only by massive investments in interconnections that cannot be undertaken by the private sector without massive support from government and/or multilateral institutions. This was the case with the natural gas connection with Romania

Gazprom extended Moldova a five-year contract under terms that are better than the country can expect from alternative resources — but worse than the terms provided to Russia’s political allies like Serbia. This is visibly aimed at depressing incentives for private suppliers and at the same time preserving the competitive advantage (economic and political) for the regimes that are loyal to Russia.

Everything now depends on how much support Moldova will get from the European Union to develop the infrastructure necessary for the country's connection to Europe’s gas grid. So far, the European Union has demonstrated robust commitment to Moldova, particularly during the gas crisis in November.

Construction: The volume of construction works in Moldova increased by 7.6% y/y in January-September, 2021. The largest segment of the market, that of civil engineering (infrastructure) works, accounting for 42% of the total in the nine-month period of 2021, stagnated. The growth was driven by the 21% advance of the volume of works for residential properties (31% in the nine-month period) while the works on non-residential buildings (25%) advanced by 7.5% y/y as well.

The significant advance of the construction activity in 2021 comes after the steadily robust performance in the previous three years. In the first three quarters of 2021, the sector accounted for 11.6% of the total gross value added generated by the country's economy. It contributed only 0.5pp to the overall 10.3% GDP y/y advance, but this is only because the sector hadn’t contracted in 2020 as industry and services did.

In the coming years, the civil engineering segment is likely to play a more substantial role in the expansion of the construction activity in Moldova, as foreign financing is being resumed.

For instance, Moldova has already negotiated a €150mn loan from the European Investment Bank (EIB) for road repairs and will negotiate a similar loan with the European Bank for Reconstruction and Development (EBRD).

The money will be used for the rehabilitation of segments of the national roads M2, M3 and M5. Previously, some of these roads were to be rehabilitated from a loan negotiated with China, while former president Igor Dodon was seeking Russian financing as well.

Major Sectors: Moldova’s agriculture offers significant investment opportunities and the local companies in the sector are growing fast as well. The edible oil production and winery segments are among the most developed, but fruit production and processing are also gaining ground. Some of the most successful Moldovan companies in the sector are those who expanded in Romania either to capture a larger market (Purcari winery, listed at Bucharest Stock Exchange) or to coordinate regional operations (Trans-Oil, which set up headquarters in Bucharest after buying assets in Serbia).

Floarea Soarelui sunflower oil producer in Balti, the largest producer of vegetable oil in Moldova and part of the Trans-Oil group controlled by Vaja Jhashi, has announced a major investment plan. In July 2021, the company announced that it would invest $30mn in a new sunoil plant in the port of Giurgiulesti where it operates a terminal. It would be the group's third plant in Moldova. It is estimated that about MDL2.5bn (€110mn) will be invested in the biggest plant in Balti. The processing capacity will increase to about 324,000 tonnes of raw material.

Swiss group Schoeni, active in the food processing and transport sectors, is investing €1.5mn in a 2,000 square metre fruit and vegetable processing plant in Moldova. The factory is scheduled for completion in May-June 2022 when it will start operating. It is the first production capacity developed abroad by Schoeni, the Swiss group that was set up in 1920. Located in the southern part of the country in Stefan Voda district, the plant will be in an industrial park developed by Free Economic Zone (FEZ) Balti.

In the first year of operations, the company, which operates through local subsidiary His East, targets a turnover of MDL18mn (€0.86mn). The output will be exported to Switzerland and other European countries.

Budget and debt

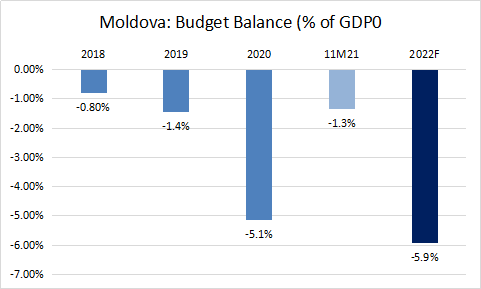

The parliament of Moldova has passed the 2022 budget,with a deficit of MDL15bn (€750mn) or 5.9% of GDP. The gap will be the biggest in recent years and notably higher than it was in 2020 when the economy faced the COVID-19 shock.

Increasing the retirement age, the resumption of external financing (from international financial institutions and the European Union) and more generous social spending are the key topics related to the 2022 budget. The retirement age for men will return to 63 years (after it was cut by the previous government to 62 years) while the retirement age for women will be gradually brought up to 63 years by 2028. Proper functioning of the pension system would require, however, a retirement age of 67 years, according to independent experts.

The public debt is planned to reach MDL103.3bn and will not exceed 40.4% of GDP at the end of 2022.

On the expenditures side, the wide deficit planned for 2022 reflects the higher social spending and higher investments in infrastructure.

Moldova’s government extended very limited social support during the first stages of the COVID-19 crisis, not least because of its limited resources. With a rather thin local public debt market and no activity on the foreign market, Moldova’s government mainly relies on its own revenues and loans from bilateral or multilateral financial institutions such as the World Bank or IMF. The previous government contemplated issuing Eurobonds, but the executive formed after the elections in mid-2021 has not resumed these plans.

The wide deficit planned for 2022 reflects on the financing side hopes for economic recovery (+4.5%) and, more importantly, expectations of robust external financing. The financing already received in 2021 from the IMF and European Union supports such expectations. At the same time, the financing from the IMF and the EU come with a calendar of reforms attached, which guarantees sustainable development.

In December, the IMF’s board endorsed the 40-month Extended Credit Facility and Extended Fund Facility (ECF/EFF) arrangements with $558mn loans attached. “The authorities’ ambitious reforms center on addressing Moldova’s longstanding and widespread governance weaknesses and institutional vulnerabilities. The proposed measures—if appropriately sequenced and resolutely implemented—are expected to yield large medium-term gains, unlocking Moldova’s untapped economic potential and accelerating its income convergence with European peers,” the IMF’s board said in the statement announcing the ECF/EFF.

The IMF also transferred $236mn to the accounts of the National Bank of Moldova in 2020, as part of the general allocation of Special Drawing Rights (SDRs) equivalent to $650bn (about SDR456bn) approved by the board of governors of the IMF on August 2, to boost global liquidity.

In June 2021, the European Commission also announced an Economic Recovery Plan for Moldova, which will mobilise up to €600mn in macro-financial assistance (MFA), grants and investments, supported by blending and financial guarantees. The EC’s plan builds on five pillars: public finance management and economic governance; competitive economy, trade and SMEs; infrastructure; education and employability; and, the rule of law and justice reform.

At the end of October, Moldova received a €60mn grant from the European Union to help with its energy crisis.

Markets

With a rather symbolic stock exchange operating in Chisinau, Moldovan companies seeking to list shares tend to consider foreign exchanges.

Moldova Agroindbank (MAIB), the biggest bank in Moldova with around 30% of the banking system’s total assets, aims to launch an IPO around 2023-24 in London, Amsterdam, Warsaw or Bucharest. The bank is already listed on the Moldovan stock exchange, however, the local bourse lacks liquidity.

Purcari Wineries became the first Moldovan company to IPO on the Bucharest Stock Exchange in 2018, and has been pursuing international expansion. In the first nine months of 2021, Purcari reported 20% sales growth, while its Ebitda margin reached 35% and net Income margin 24%.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now

_1783009797.jpeg)