Rheinmetall to more than double gunpowder output at Bavaria plant

1 day ago

Who is going to pay for rebuilding Ukraine after the war is over? Now the EU has raised a €90bn two-year loan to keep the country in the fight against Russia, attention has started to turn to what comes next. The European Commission (EC) has drawn up a draft recovery plan for 2028-2034 but it falls badly short of what is needed: the proposal calls for €405bn of investment; the EU is offering €89bn – some €300bn of reconstruction funds are missing.

The European Commission's proposed Ukraine Reserve under the EU's next seven-year budget framework published in April pencils in around €13.5bn annually – between half and a third of what is needed.

The briefing, written by Dmytro Boyarchuk of the Centre for Social and Economic Research and fellow Marek Dabrowski, puts the minimum public funding requirement for ten years of post-war recovery and reconstruction at €196.5bn — more than double what the Commission has proposed. The gap of more than €100bn over the seven-year MFF period represents the most significant tension in the EU's planning for Ukraine since the invasion began.

The scale of the damage

Calculating the amount of damage that needs to be repaired is a tricky task. The World Bank recently increased its estimate to $587.7bn, but that is the cost of reconstruction over ten years. The World Bank’s estimate of just the physical damage is $195.1bn, almost the same as the EC’s estimate.

The calculation is further complicated by the fate of the regions occupied by Russia. Currently the Armed Forces of Russia (AFR) controls a bit less than 20% of Ukraine’s territory. If a peace deal is done then it is highly likely that most of that territory will remain under Russia’s control – and the Kremlin will be responsible for paying for its reconstruction.

Indeed, Russia controls the Black Sea port city of Mariupol and has already poured RUB100bn ($1.1bn) into its reconstruction, according to Russian reports. At the same time various Russian government programmes for occupied parts of Donetsk, Luhansk, Zaporizhzhia and Kherson regions together run into several hundred billion rubles.

As most of the fighting took place in eastern Ukraine in what are now occupied territories, the lion’s share of the rebuilding costs will fall on the Kremlin, not Bankova. Before the war, Mariupol had a population of about 430,000 and suffered some of the most extensive urban damage of any Ukrainian city. The cities in the west of the country, still under Kyiv’s control, have suffered far less.

Interestingly, at one point in the last year of talks with the US, Russian President Vladimir Putin suggested that the frozen $300bn of Central Bank reserves could be used to pay for reconstruction – as it appears the Kremlin never expects to get this money back – but only if part of the funds were used to pay for the reconstruction of Russian-held territory in Ukraine. That idea was enshrined in Trump’s proposal for a $100bn Ukraine investment fund using the CBR money that was included in the 27-point peace plan (27PPP) thrashed out at the Moscow meeting on December 3. Now the EU has taken over the lead in ceasefire talks with Moscow, that idea has been abandoned.

Mountain to climb

Even if the money can be found, as IntelliNews reported, Ukraine will still have a mountain to climb as nearly every sector of the economy has been damaged by the war.

The starting point is the destruction already inflicted. The Fifth Rapid Damage and Needs Assessment (RDNA5), published in February 2026 by the World Bank, European Union and United Nations, estimate of $195.1bn is a lower estimate as it excludes the four most heavily contested eastern and southern oblasts of Donetsk, Luhansk, Zaporizhzhia and Kherson which have suffered an addition $99.6bn (€88.3bn) of damage.

The sectoral breakdown of damage in government-controlled territories is led by housing at $28.3bn, followed by energy infrastructure at $21.7bn, transport at $17.4bn and commerce and industry at $9.6bn. For example, pre-war Ukraine had 57GW of generating capacity; following last winter’s Russian bombardment only 10GW remains undamaged.

But war damage figures are only the starting point. The "Build Back Better" principle — which means rebuilding to higher standards of energy efficiency, seismic safety and protection against air strikes rather than simply restoring what existed before — substantially increases the cost. The RDNA5 estimates total recovery and reconstruction needs over ten years at $587.7bn (€520.8bn). The authors' own more conservative estimate, which assumes a significant share of private investment across energy, housing and transport, puts the total at $457.1bn (€405.1bn).

Who pays for what

The briefing draws a careful distinction between what public money should fund and what the private sector should finance. Public funding of €82.2bn would cover infrastructure and public goods — transport networks, electricity grids, pipelines, communal infrastructure, social housing, healthcare and education — which are unlikely to attract private investment.

A further €228.4bn in mixed public-private funding would be required for energy, housing and transport sectors where state guarantees and risk insurance could catalyse private capital. The remaining €94.4bn is expected to come from purely private sources — domestic and foreign investment in industry, agriculture, telecommunications and services.

The critical assumption is that private investors will actually deploy that capital. At the recent EBRD meeting in Riga the UK’s Chancellor of the Exchequer Rachel Reeves said that London plays a key role in facilitating this investment by helping to build war insurance coverage to encourage private investment into a post-war Ukraine. Reeves was upbeat about the prospects for war insurance, which has emerged as the leading mechanism to facilitate this private investment, but admitted that work on structuring effective war insurance has only just begun and what is currently available is woefully inadequate.

The emerging market investors and fund managers IntelliNews has talked to all agree that Ukraine is one of the best investment stories in the Former Soviet Union (FSU) as it still has most of its “catch up” story ahead of it. However, they also say they would be reluctant to invest until there has been a wholesale reform of the judicial system and strong property rights have been introduced. On top of that there is the political risk of a second invasion by Russia and it would probably take years of peace to mitigate those fears.

A lot will depend on how succesful the West is in providing Ukraine with solid security deals that both the US and the EU have been very reluctant to provide. EU membership for Ukraine would solve the security deal problem, thanks to its Article 5-like collective security arrangements in Article 42/7 of the EU founding treaty, but Ukraine’s accession is unlikely to happen for a decade, if then.

If security guarantees are weak, the reform process stalls or Ukraine’s EU accession slows, the private investment assumption becomes optimistic — and the public funding requirement rises accordingly.

The EU's proposed budget: some, but not enough

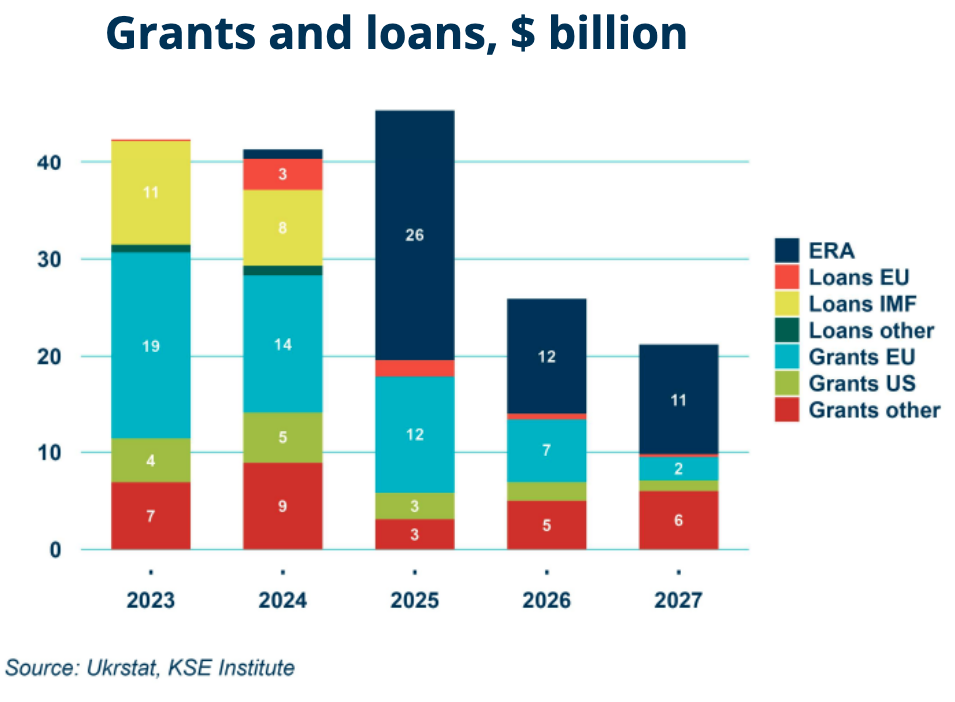

Against this backdrop, the Commission's €88.9bn Ukraine Reserve for 2028-2034 is the central object of the briefing's critique. The authors note that the proposed allocation is smaller than the €193bn of EU and individual support for financial, military and humanitarian assistance sent to Kyiv since February 2022 – not including the most recent €90bn EU loan – much of it in the form of loans. Ukraine's sovereign debt now exceeds 100% of GDP — reaching 108.7% at the end of 2025 according to IMF data, up from around 35% pre-war.

The debt figure matters enormously for how the aid is structured. Given the very high level of Ukraine's sovereign indebtedness, official recovery and reconstruction aid should predominantly take the form of grants. The dominant role of lending in the current EU proposal ignores the current debt position — loading further loans onto a country already at 108.7% debt-to-GDP would add unsustainable pressure to an already stressed fiscal position.

The prospect of the EU giving Ukraine grants (free money) instead of loans (that need to be repaid eventually) is not good. For the first three years of the war the Biden administration was very generous, largely giving Ukraine grants rather than loans, but the EU has always made loans in preference to grants. However, since US President Donald Trump took office, the US has sent no more money to Ukraine, leaving the EU to take up the entire burden.

Since 2025 the mechanism for support has changed with the introduction of the G7’s Extraordinary Revenue Acceleration (ERA) Loans for Ukraine mechanism. The EU's share is approximately €18.1bn. That provided an additional $50bn in financial assistance over 2024-27, serviced by the profits from the CBR’s frozen sovereign assets and structured to prevent fiscal liability by Ukraine. That facility has been almost exhausted and will be replaced by the €90bn loan agreed in December, but both the grants and loans from the EU are already drying up thanks to an increasingly dysfunctional European economy. As IntelliNews reported, Russia’s economy is under pressure, but so are everyone else’s economies in the EU.

In addition, the Ukraine Facility set up in 2024 and funded from the EU budget, which governs disbursements for 2024-2027, provides €50bn in loans and grants. The proposed MFF allocation of €88.9bn for 2028-2034 would represent a sharp reduction in the annual run-rate of EU support at precisely the moment that post-war reconstruction is expected to begin in earnest.

The absorption problem

Even if sufficient funding were committed, Ukraine could not spend it instantly. Drawing on research covering 27 post-conflict economies, the briefing estimates Ukraine's maximum aid absorption capacity at around 20% of GDP at current exchange rates — equivalent to approximately $42bn or €37.2bn annually in 2025 terms. This means the recovery and reconstruction process will inevitably take several years beyond the end of the MFF in 2034.

Ukraine's administrative capacity to manage the reconstruction process is also a constraint. The country's track record on anti-corruption has been uneven, and the ongoing $100mn Energoatom corruption scandal that has implicated almost all of Ukrainian President Volodymyr Zelenskiy inner circle has raised fresh worries about the robustness of oversight mechanisms.

The briefing argues that conditions attached to EU aid should go beyond EU accession-related reforms and macroeconomic discipline to include far-reaching reforms in public administration, law enforcement bodies and the judiciary – precisely the “fundamental cluster” of EU accession reforms where Bankova has made the least progress.

Just this week the EC said that Ukraine risks losing more than €680mn in EU funding under the Ukraine Facility due to delays in implementing reforms. Brussels has suspended €300mn from the fourth tranche and over €380mn from the fifth tranche pending completion of anti-corruption and judicial reforms. If the reforms are not completed by the June 30 and September 29 deadlines, the European Commission could permanently reduce the payments, although some flexibility remains because of the war.

The population question

A further complication is the baseline population on which reconstruction planning must be built. The briefing assumes a post-war recovery will be conducted on territory under Ukrainian government control as of April 2026, with a population of approximately 32mn — down significantly from Ukraine's pre-war population of 44mn. Other recent estimates put the number even lower at 25mn people as Ukraine is suffering from the worst demographics in the world – nearly half of the population left in the country are now pensioners.

The research suggests that only a portion of the approximately 6.5mn-8mn Ukrainian refugees in Europe will choose to return, though the exact share is uncertain and highly sensitive to security conditions and economic prospects. Moreover, according to some analysts, as soon as martial law restrictions on men leaving the country are lifted post-war, millions of Ukrainian men may leave to join their families now living in EU countries like Poland and Germany making the demographics even worse.

A smaller population means a smaller tax base, a reduced labour force for reconstruction, and a lower long-term growth trajectory — all of which affect the viability of the private investment assumptions that underpin the briefing's cost estimates.

The war complication

The briefing explicitly acknowledges that all its estimates depend on a war that is still being fought. As long as the war continues, large-scale reconstruction does not make sense — it would mean the waste of aid resources. Only repairs to energy, transport and social infrastructure are warranted during active conflict. The longer the war continues, the more the damage, recovery and reconstruction needs will increase.

The MFF must therefore be designed for two scenarios simultaneously: one in which a ceasefire or peace agreement arrives before 2028 and full reconstruction can begin; and one in which the war is still ongoing when the new budget period starts. The draft MFF legislation is flexible enough in this respect, but the proposed budget allocations remain insufficient under either scenario.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now

_14_1784882957.jpg)