_1.png)

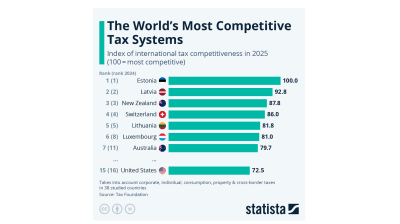

Estonia has the world’s most competitive tax systems for the 11th year in a row – STATISTA

2 hours ago

Russian services activity stabilised in August after two consecutive months of decline, according to S&P Global’s latest PMI data, but the broader private sector continues to face subdued demand and weakening confidence. (chart)

The seasonally adjusted S&P Global Russia Services PMI Business Activity Index posted 50.0, the no-change benchmark, in August, up from 48.6 in July. The reading follows contractions in June and July. S&P Global noted that “some companies continued to highlight subdued demand conditions,” but added that “a slower fall in new business contributed to a stabilisation in output.”

Despite persistent weak demand, employment in the services sector rose at the fastest pace since February. “Firms reportedly sought to boost capacity amid anticipated expansions in sales in the coming months,” S&P Global said in its report published on August 30. The modest increase in hiring helped keep backlogs broadly stable, ending a nine-month run of growing work-in-hand.

Input cost inflation moderated significantly, with companies reporting the joint-slowest rise in input prices in over five years, alongside June 2025. “More favourable exchange rate movements helped slow the rate of inflation,” according to survey respondents. However, the rate of increase in output charges accelerated for the second month running. S&P Global said the pace of inflation was “the joint-fastest since January,” as firms sought to pass on rising costs from utilities and suppliers.

The broader Russian private sector remained under pressure, with the S&P Global Russia Composite PMI Output Index registering 49.1 in August, up from 47.8 in July. Manufacturing activity continued to decline, albeit at a softer pace, with the headline PMI for the sector rising to 48.7 from 47.0.

The PMI picture is mildly improved and can be taken as sign that the Central Bank of Russia (CBR)’s policies of slowing the economy to reduce inflation so it can cut rates may be starting to have some beneficial effects.

CBR governor Elvia Nabiullina introduced a non-traditional policy of artificially slowing growth last August using non-monetary policy methods that has caused a sharp slowdown this year. But the upside is that sticky inflation in 2024 has begun to fall and is falling faster than expected.

That has allowed the CBR to put in 300bp of rate cuts since July and the regulator says it hopes to put in another 300bp of growth-boosting cuts before the end of the year that would bring the prime rate to a more manageable, but still high, 15%. In its latest Talking Trends newsletter, the CBR says its still targeting an inflation rate of 4%, but that it will take several years to reach that goal.

New orders across both sectors fell for a second consecutive month. The decline was described as “slight,” with companies attributing the contraction to “challenging financial conditions and customer hesitancy.”

Confidence in the year-ahead outlook also weakened. While service providers still expect output to rise over the coming 12 months, optimism slipped to its second-lowest level since July 2023. “Hopes of stronger demand conditions and expansion into new markets underpinned positive sentiment,” the report said, though the overall level remained below the long-run average.