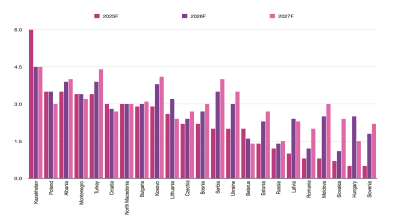

Emerging Europe’s growth holds up but risks loom, says wiiw

1 hour ago

Following the collapse of Iran's troubled Ayandeh (Future) Bank and its absorption into Bank Melli Iran, attention has now turned to the bank's former management after years of difficulties.

Ali Ansari seemed to have the Midas touch. Born in Tehran in December 1962 to a construction family, he rejected the family business of residential building to strike out on his own. With his father's support, he obtained a licence from Zanjan's heavy industries department to manufacture pipes and profiles. In 1993 he opened a factory in Mahdash, Karaj — the foundation of his fortune.

Success bred ambition. Ansari entered the fruit and dried fruit trade, eventually exporting to the Caucasus and Azerbaijan. In 1994 he established Bazar Ahan Shadabad, a distribution centre for iron and steel in Tehran's Shadabad district that became one of Iran's largest metals trading hubs. The facility later changed its name to Behadaran Commercial Complex.

When mobile phones became widespread in Iran during the mid-2000s, thanks to credit lines from Irancell and Mobile Communications Company of Iran (MCI), Ansari spotted another opportunity. In 2006 he opened Iran Mobile Market. The public rushed to buy handsets, swelling his wealth to the point where he appeared on lists of Iran's richest individuals, Etemad newspaper reported about the banker on October 23.

He applied the same formula to furniture retail, opening Bazar Meubles. The venture transformed the area's economy, spawning hundreds of shops and independent businesses. Ansari became chairman of the furniture and decoration trade association. Yaft Abad market is now considered among Tehran's most luxurious shopping centres.

His involvement with popular Esteghlal Football Club's board during the 2000s, and his appointment as chairman of Iran's cycling federation in August 2009 with 39 votes, raised his public profile further. He owned Iran Mall, confirmed as the world's largest shopping centre, near Lake Chitgar, which houses car showrooms, cinemas, hotels, restaurants, waterfalls, ice rinks and tennis courts. He refused to sell units, only leasing them.

Yet Ansari's banking ventures would prove disastrous. In 2009 he co-founded Bank Tat with former managers from Kesharvazri Bank and Export Bank. Regulators accused the founders of failing to provide required capital, allegedly submitting just one-tenth of the legal minimum through property collateral rather than cash. Three years later Bank Tat declared bankruptcy.

The wreckage was hurriedly swept together. Bank Tat merged with Saleheen Credit Institution and Ati Credit Institution to form Ayandeh Bank in 2014, with Ansari as principal shareholder. But the new lender replicated its predecessor's failings. From establishment, Ayandeh Bank allocated over 90% of deposits to related parties and projects under the bank's own management, according to Hamidreza Ghani-Abadi, director-general of banking supervision at the Central Bank of Iran. Iran Mall, Mashhad Mall, Rotana Hotel and Farmaniyeh Mall were among the main projects Ayandeh Bank financed.

The funds never returned. To pay interest on existing deposits, Ayandeh Bank attracted fresh deposits by offering rates six to seven percentage points above the banking system average, what regulators described as a Ponzi scheme, criminal in other jurisdictions. When the network average stood at 18%, Ayandeh paid 26-27%. When competitors offered 23%, Ayandeh paid 31-32%. The strategy poisoned the entire banking sector, forcing rival lenders to breach central bank regulations to retain deposits.

The authorities removed management in late 2019 and launched a reform programme. Transparency efforts revealed the bank's true ownership structure, which had previously been concealed through proxies. But the damage was irreversible.

In 2022, the Iranian criminal court indicted dozens of individuals including senior bank executives including Ansari, government officials and businessmen on charges of disrupting the economic system through banking fraud and embezzlement, according to a court document leaked at the time. Accordingly it said, Branch 1059 of Tehran's Criminal Court issued the indictment against officials from the Ministry of Economic Affairs and Finance, Police Intelligence and Security, Bank Ayandeh (Future Bank), Bank Melli and various other entities.

The indictment accused the defendants of using their positions to obtain illegal loans through manipulation of the banking system, creating disruption in the banking sector, and interfering in the land registration system. The charges also included embezzlement through various fraudulent schemes and money laundering operations designed to disrupt the banking system.

By October 2025, Ayandeh Bank had accumulated IRR550 trillion ($503mn) in losses against registered capital of just IRR1.6 trillion. Overdrafts from the central bank reached IRR500 trillion. The capital adequacy ratio, legally required to reach 8%, had plunged into negative territory, according to local outlet Didban.

On October 23, regulators placed Ayandeh Bank into resolution. Bank Melli Iran, the state lender, will absorb IRR267 trillion in deposits and all employees. Unaffiliated shareholders can settle at the highest share price over the past year, or wait for asset liquidation. Ansari's projects, those monuments to ambition, will be liquidated to repay creditors, Tasnim previously reported.

To add insult to injury to the depositors of Ayandeh, Ansari was not sentenced despite the string of failures of the banking system, unlike counterpart billionaires like Babak Zanjani at one point facing the death penalty for his dealings in oil exports which earned him his fortune. Like his counterpart, his level of impunity has caused trouble for the government following successive administrations and local city municipality mayors backing his activities.

Unfortunately for the CBI, the Ansari scandal continues to raise questions over the entire banking system which has suffered from years of poor management and shocks from US and EU sanctions. The Iranian rial remains historically low against the dollar, while the entire economy remains on life support with interest rates stubbornly high making loans almost impossible to attain.