Ben Aris in Moscow -

There has been a spate of articles recently suggesting that Russia is on the edge of a complete economic meltdown. There was an article in the UK's The Daily Telegraph suggesting that its economy has lost a third of its value in dollar terms and dropped from eighth largest economy to 13th largest on a par with Spain. Then The Economist ran a cover story claiming that, "Russia is closer to crisis than the West or Vladimir Putin realize," because it was running out of money. And most recently Professor Anders Aslund of the Peterson Institute for International Economics wrote a blog suggesting that nearly $200bn of Russia's hard currency reserves somehow "don’t count" and that it doesn’t have enough money to meet its debts.

To be clear: Russia is not in crisis. It is going through a very painful adjustment caused by tanking oil prices, but its economic fundamentals remain extremely solid – far better in fact than most of the countries in Western Europe, let alone the rest of the Commonwealth of Independent States (CIS). It is Ukraine that is on the verge of an economic meltdown.

Professor Aslund wrote in an op-ed on December 1 entitled "Russia's Economic situation is worse than it may appear", and followed up a week later with "The Russian Economy is headed for disaster." In both pieces he claims that the Central Bank of Russia’s (CBR) $420bn reserves number is a fiction and actually it only has $203bn in "useable" money.

Drilling down into the $420bn number, Aslund says: "Of this amount, $45bn is held in gold, and $172bn in the two sovereign wealth funds, the Reserve Fund and the National Wealth Fund. The Ministry of Finance controls those two funds, much of which is deposited in state banks or invested, so these funds are not liquid reserves. If we deduct gold and sovereign wealth funds, the official reserves shrink to $200bn. In the last year, Russia's international reserves have declined by $103bn. In the coming year, they are likely to fall by another $100bn, because Russia has to pay back about $150bn a year, while its current account surplus is about $60bn a year. When the market realizes that Russia's reserves are running short, capital outflows will accelerate in anticipation of capital controls and the exchange rate will fall further."

Aslund's numbers also deserve closer examination:

• $45bn is held in gold: Aslund argues that because these reserves are in gold, they are not liquid and so can't be counted as reserves. Firstly it is completely normal for countries to hold part of their reserves in gold as a hedge against currency movements. Russia holds just under half of its reserves in euros, which have done poorly against the dollar this year, so holding something else, like gold, is actually a plus. Moreover in times of crisis – and Russia going into default would not only cause turmoil on European markets, but would cause several CIS countries like Tajikistan and Armenia to collapse, possibly sparking an Asian-style global crisis – gold's value goes up. And as the international bullion market is worth $2.5tn – twice the size of the UK Gilt market – to suggest gold is not a liquid asset is risible.

• $172bn in the two sovereign wealth funds: this is a more valid point. The funds are under the control of the Ministry of Finance, but as to "much of which is deposited in state banks," this part is unclear. There are very strict rules on how this money can be used and while this money may be less liquid than the CBR reserves, Moody's Investors Service says most of this money is on account in the CBR and is confident it is available if needed. Looking at this issue from a different perspective, the CBR is currently providing the bulk of liquidity to the bank sector to the tune of about RUB7tn, or $140bn, but this is provided in rubles, which the CBR can print if it needs and those dollars can be made available if needed.

• $103bn decline in international reserves: this is true. But in the last year the ruble was still in the exchange corridor and the CBR was obliged to defend it. However, from December the currency is now truly freely floating. Traders have been freaked out by the fact that the CBR is not intervening much, the whole point of which is to preserve Russia's hard currency reserves. So the proposition that, "in the coming year they will likely fall by another $100bn," is questionable.

• $150bn of debt Russia has to pay in 2015: is the reason reserves have to fall. However, more than half of this debt ($90bn) is owned by just two state-owned companies, Rosneft and Gazprom, both of which earn hard currency for their exports and both of which are able to pay their debts out of their cash flow, so this will have no impact on the CBR's reserves. The current account surplus is enough to cover the rest. In any case, Russia's companies and banks have spent this year building up hard currency reserves and according to Moody's are already in a position to meet their obligations. Aslund himself quotes JP Morgan, which estimates Russian banks have accumulated $292bn in foreign assets, but speculates without proof that this belongs to the sovereign wealth funds, ignoring the fact that this sum is actually $120bn more than those funds collectively hold.

• $120bn net capital outflow: Aslund names this number elsewhere in his articles and it is true that capital outflow is running much higher this year – almost double the level of last year. However, drilling into this number and it is not quite so scary. Firstly, Russia is a net exporter of capital, and always has been, as it invests more money overseas than it receives as investment – mostly in the other CIS countries. This "capital flight" has been running at about $50bn a year for a decade. Secondly, a quirk of Russia's accounts mean that the profits earned by these Russian-owned firms abroad that are reinvested in these foreign companies are counted as "capital flight" too – almost no other country does this – and runs at some $20bn a year. And finally, after slowing down in the middle of this year "capital flight" took off again in the third quarter to the tune of just under $30bn. But this was exactly the same time as Russia was cut off from the international capital markets by the EU-US financial sanctions. In other words this is not Russian money fleeing a collapsing Russia, but simply companies that are unable to refinance their debts so paying them off with cash instead, argues Evgeny Gavrilenkov, chief economist at Sberbank, thus reducing Russia's vulnerability shocks even further from an already low level. It should also be noted that even if total "capital flight" this year is $120bn, this is still only 6% of GDP – well down on the approximately 15% Russia was losing a year in the 1990s when capital flight really was capital fleeing the country.

This whole article and many similar articles are full of Schadenfreude, scaremongering or raw, unjustified speculation that assumes a collapse.

Take this paragraph for example: "Russia has no problem with its budget balance, its public debt, or its current account. They all look rock solid. Yet we are seeing the beginning of a depreciation-inflation cycle and economic decline. The Central Bank of Russia will be forced to raise interest rates further to limit both inflation and depreciation. A fall in the oil price of 40% means that Russia’s exports will fall by 20% or $100bn, which will reduce investment, consumption, and GDP. Although Russia’s banks are considered to be well capitalized, many banks are bound to suffer from currency mismatches and the ever-cheaper ruble. The costs of bank failures are bound to end up on the state budget."

If you strip out the speculation, you are left with this: "Russia has no problem with its budget balance, its public debt, or its current account. They all look rock solid… Russia’s banks are considered to be well capitalized." So citing Aslund's own facts, the Russian economy is strong and so are its banks.

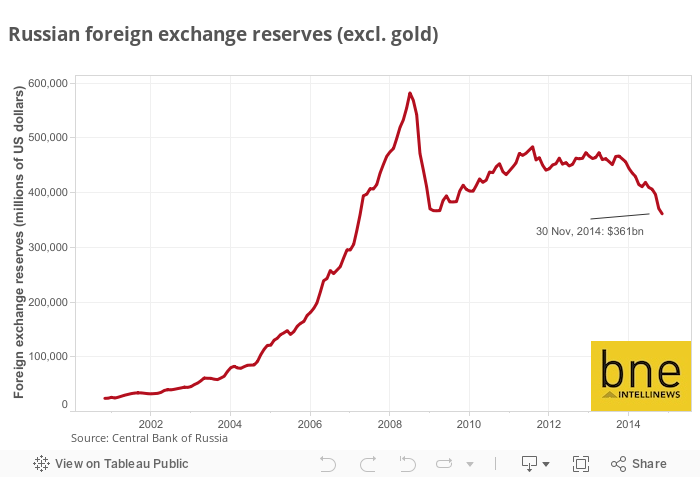

To finish, Moody's issued a report on December 5 entitled "Foreign Exchange Reserves Decreasing but Sufficient to Cover 2015 External Debt Needs."

It said: "According to official data, the Bank of Russia (CBR)'s [foreign currency reserves] (as of 1 December 2014) are at $361bn. This is more than sufficient to cover the country's external debt payment obligations through 2015, which amount to roughly $130bn across government, banks and corporate debt. That assumption holds even when excluding the $150bn of FXRs counted as the central bank reserves that come from the government's two special savings Funds – the National Wealth Fund (NWF) and Reserve Fund (RF). While these two Funds have specific mandates and are therefore unlikely to be used either to intervene in the foreign exchange market or to finance the government's external debt payments, like the CBR's own reserves, the amounts placed in the central bank contain liquid, marketable assets, that can be utilized if required."

Why don’t the anti-Russia crowd just confess that what it is passing off as "analysis" is actually wishful thinking?

Related Articles

Drum rolls in the great disappearing act of Russia's banks

Jason Corcoran in Moscow - Russian banks are disappearing at the fastest rate ever as the country's deepening recession makes it easier for the central bank to expose money laundering, dodgy lending ... more

Kremlin: No evidence in Olympic doping allegations against Russia

bne IntelliNews - The Kremlin supported by national sports authorities has brushed aside "groundless" allegations of a mass doping scam involving Russian athletes after the World Anti-Doping Agency ... more

PROFILE: Day of reckoning comes for eccentric owner of Russian bank Uralsib

Jason Corcoran in Moscow - Revelations and mysticism may have been the stock-in-trade of Nikolai Tsvetkov’s management style, but ultimately they didn’t help him to hold on to his ... more

Most Read

-

Putin to skip Rio BRICS summit over ICC warrant as Xi signals no-show

15 days ago

-

Turkey yet to prove rare earth deposit has suggested “giant” potential despite reported processing talks with China

10 months ago

-

Uproar in Mongolia as development bank reveals scale of risky loans and NPLs

3 years ago