COMMENT: Czechia economy powering ahead, Hungary’s economy stalls

4 days ago

The war in Ukraine is likely to drag on for years but from 2023 onwards the impact will increasingly be limited to the combatants themselves and countries in Russia’s immediate neighbourhood, Fitch Solutions analysts told a webinar on April 18.

This is in contrast to the year following the invasion, when the global economy was affected by the hike in prices of energy and other commodities, which fuelled an inflationary spiral, causing a dramatic slowdown in growth.

Anwita Basu, head of Europe country risk at Fitch Solutions, commented that sentiment about global and European economies has improved, with the market consensus on growth for 2023 now on an upward trend.

“Most forecasters have moved past [the] idea of a full-year recession in Western economies,” she told the webinar. While acknowledging that “we remain cautious of this new-found optimism”, Basu said that measures of economic activity in the Eurozone have shown signs of a pickup, with industrial activity now increasing.

No end in sight

In the Europe Macroeconomic Update: Paths Unknown webinar, organised by Fitch Solutions company BMI on April 18, analysts were pessimistic on the future of the war in Ukraine, forecasting it will last at least until the end of 2023, if not longer.

“Our core view is that the war in Ukraine will continue for several years, at various degrees of intensity,” said Lucinda Ritchie, lead Russia analyst, Europe country risk at Fitch Solutions.

“We think the current phase will continue to 2024, and will be characterised by a grinding war of attrition, with neither side able to fulfil their war objectives … From 2026 onward, a state of frozen conflict will set in.”

However, said Basu, as the war continues, Fitch Solutions expects “the impact to be isolated to the countries involved, which is mainly Russia, Ukraine and Belarus, and countries faced with trade flow restrictions to due to the war such as Armenia, Georgia and the Central Asia region.”

Ritchie agreed that the “direct impact [of the war] is becoming more localised to Central Asia and the Caucasus”. However, she adds, across Europe “the war in Ukraine will be an ongoing and pervasive factor affecting policy decisions and macro conditions for years to come”.

For the combatants, the economic damage is already evident, as shown by full-year 2022 figures for Russia and Ukraine.

Ukraine’s economy contracted by 29.1% following the outbreak of war, and is expected to post positive growth of just 0.4% in 2023.

For Russia, meanwhile, a longer war will only prolong its economic isolation and lower growth potential, says Ritchie.

“Without a political resolution, we expect sanctions to be in place until at least 2030,” she said. “There is little scope for rapprochement with the West when Putin in power.”

Another factor in Russia is the impact of military recruitment on the civilian economy. On top of the estimated 900,000 Russians that emigrated in 2022, 300,000 were mobilised in September 2002 and a further 147,000 are expected to be drafted in April-July this year, and a similar number in September.

“Roughly 1.5mn people will be out of the civilian economy and labour force in just over a year,” said Ritchie. This has consequences for inflation as well, she explained. “We expect the supply of goods and labour to tighten as military recruitment shrinks the labour force, causing output to stagnate and inflation to continue building.”

Inflation still a concern

For the rest of Europe, sub-regional factors such as the European Central Bank’s (ECB) rate-setting decisions or elevated political uncertainty in Central Europe will have a more important effect on growth in 2023 than the war, Basu forecast.

Sentiment in Europe has improved, despite taking a temporary hit from the recent crises at Silicon Valley Bank (SVB) and Credit Suisse. High frequency data in Europe has been mixed, as Fitch Solutions analysts pointed out, with inflation remaining well above the ECB target of 2%.

“External price pressure on the eurozone is weakening, but internal pressures remain a concern,” said Jonas Decker, associate analyst at Fitch Solutions.

“Lower energy prices caused a deceleration of headline inflation, but we believe declining energy prices obscured continuing price pressures … What was once external inflation is starting to seep into the fundamentals of European economies.”

He sees the ECB as unlikely to end the current tightening cycle despite lower headline inflation.

In Central Europe, where many of the economies remain outside the eurozone, central banks stepped in earlier to tackle inflation, with some launching their tightening cycles as early as 2021.

“Our core view for Central European monetary policy is for rates to remain on hold throughout 2023, as they are already at very restrictive levels, before starting to come down in 2024,” forecast Adrian Terzic, senior analyst at Fitch Solutions.

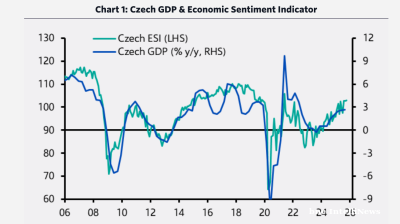

“Depressed economic outlooks in the region will act as a constraint to policy-makers this year. We expect annual GDP contractions in Hungary and the Czech Republic and only modest growth in Poland and Romania. In this context, further rounds of tightening would add additional strain to the growth outlook, which is feeling the pinch from an already tight monetary policy backdrop and also still elevated inflation.”