NYT details institutional corruption in Zelenskiy’s government

11 hours ago

The world order is changing. The emerging markets are coming of age and they are setting up a raft of largely non-Western Global Emerging Markets Institutions (GEMIs) to coordinate their lives.

An alphabet soup of organisations has emerged – BRICS+, G20 , the Shanghai Cooperation Organization (SCO), Eurasian Economic Union (EUU), ASEAN (Association of Southeast Asian Nations), the African Union, to name a few – but unlike their Developed Market (DM) peers, these organisations remain immature and are still in the process of working out what they want to achieve. In the meantime, what is holding them together is trade, dominated by China.

APPENDIX: Leading Global Emerging Markets Institutions (GEMIs

Since the advent of US President Donald Trump the world has gone through a profound change. A new economic paradigm has emerged based on the transactional multipolar world model that the US president has introduced, highlighted by his Liberation Day tariff scheme. Geography has reasserted itself in an increasingly fractured world. The old alliances, especially in the Global North, now count for nothing where the US seeks to maximise its profits, often at the expense of its traditional partners.

The big difference between the Global North and South is that the new markets are pragmatically focusing on economic and trade relations. Both Chinese President Xi Jinping and Russian President Vladimir Putin have adopted a strict policy of non-interference into domestic affairs (at least publicly), as they outlined in a joint 8,000 word essay last year. Given that many countries, notably the African Continent and India, still see the DMs as neo-colonialist powers, this stance appeals strongly to the new world. As bne IntelliNews reported, the Moscow consensus emerged early in Putin’s reign, which demands the citizens put the interests of the state ahead of their own, in sharp contrast to the Washington Consensus that has individual happiness and prosperity at its core. Human rights abuses and political repression are legion in Russia and China, but are off limits in mutual relations, whereas the DMs take it on themselves to criticise, sanction and even bomb any GEM country they deem to be acting beyond the pale. The point was most recently illustrated by Trump’s decision to impose 50% sanctions on both India for importing Russian oil and Brazil over the Bolsonaro case – both politically motivated decisions.

It has become a dog-eat-dog world and the GEMIs have adopted the obvious strategy: ignore the US and increase trade with each other. This process was already underway under the Biden administration with the emergence of a BRICS bloc, where trade has been flourishing, but Trump has rapidly accelerated the process. Political analysts argue that the US has made a huge geopolitical blunder by pushing the largest GEMs together – most notably Russia, China and India – which are not natural allies, but have been forced to increase cooperation in the face of an increasingly aggressive America.

Biggest market in the world

Trade relations are suddenly in flux. Putin has taken the extreme step of breaking off relations with the West entirely and has become the most sanctioned country in the world as a result. He has made a big bet on the Global South Century so far successfully completely swapping trade with the West with booming economic relations with new GEM partners. Within the space of only four months, he managed to entirely reorient Russia’s oil exports from Europe to Asia after the twin oil sanctions came into effect at the end of 2022. And the effort to isolate Russia has largely failed; Putin was the guest of honour at the recent Shanghai Cooperation Organization (SCO) summit in China, surrounded by leaders from many of the biggest markets in the world, including China’s Xi, and India’s Prime Minister Narendra Modi.

The combined BRICS+ and SCO grouping now encompasses more than 5.26bn people—approximately 64% of the world’s population—and accounts for an estimated 55% of global GDP based on purchasing power parity (PPP), according to 2025 projections from the International Monetary Fund. Likewise, the recent tie up between the Gulf Cooperation Council (GCC) tied up with ASEAN (Association of Southeast Asian Nations) in May creates a market of over 2bn people, 30% of the world's GDP and, crucially, about 55% of world GDP growth in PPP terms. And there are dozens of these cooperative deals amongst the GEMs.

|

Selected GEMIs vs Developed Markets: GDP and population |

||||||

|

Organisation |

Share global GDP (PPP) % |

Share global GDP (Nominal USD) % |

GDP (PPP, USD trillions) |

Nominal GDP (USD trillions) |

Members’ population (millions) |

Share of world population % |

|

BRICS |

37.5% |

26.8% |

79 |

32 |

3,950 |

49.3% |

|

SCO |

34.2% |

22.1% |

72 |

26 |

3,420 |

42.7% |

|

BRI |

42.0% |

28.5% |

88 |

34 |

5,340 |

66.7% |

|

G20 |

85.0% |

82.3% |

179 |

97 |

4,950 |

61.8% |

|

EAEU |

4.0% |

3.2% |

8.4 |

3.8 |

185 |

2.3% |

|

ASEAN |

6.8% |

5.1% |

14 |

6.0 |

685 |

8.6% |

|

MERCOSUR |

2.9% |

2.4% |

6 |

2.8 |

295 |

3.7% |

|

G7 |

29.8% |

44.5% |

63 |

53 |

775 |

9.7% |

|

EU (27) |

16.5% |

15.8% |

35 |

19 |

448 |

5.6% |

|

NATO |

33.1% |

44.3% |

70 |

52 |

981 |

12.3% |

|

Sources: IMF World Economic Outlook (April 2025) for GDP (PPP and nominal); UN Population Division (2024 revision, mid-2025 estimates) for population. Global PPP GDP ~$210 trillion; nominal ~$118 trillion |

||||||

Just the BRICS+ and SCO includes full members, observer states, dialogue partners, and potential future members, spanning over 30 countries across multiple regions. The bloc’s estimated GDP of $151 trillion in PPP terms dwarfs the US’ $30 trillion and the EU’s $18 trillion.

The G20 is even bigger, with a total GDP nominal value of $97 trillion and PPP adjusted value of $179 trillion. By comparison the G7 has a nominal GDP worth of $53 trillion and an adjusted value of $64 trillion.

The organisers of the SCO described it as a “global powerhouse” in oil, technology, trade, and de-dollarisation efforts. The overlapping BRICS+ and SCO memberships is a coordinated shift in geopolitical and economic influence away from traditional Western-led structures to the new world.

The BRICS+ grouping—comprising 10 full members and 10 partner countries, not counting another dozen candidate countries—includes Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Iran, the United Arab Emirates, and Indonesia, alongside partner states such as Belarus, Bolivia, Kazakhstan, Cuba, Malaysia, Nigeria, Thailand, Uganda, Uzbekistan, and Vietnam. In total, BRICS+ covers approximately 4.45bn people and contributes $76 trillion to global GDP, or 44% of the total, more than double the core group of five. And with Indonesia’s addition in January, the fourth most populous country in the world, the group will continue to grow.

The SCO, originally established as a regional security bloc, now includes 10 full members and 17 observers and dialogue partners. Its core membership includes China, Russia, India, Kazakhstan, Pakistan, Iran, Uzbekistan, Tajikistan, Kyrgyzstan, and Belarus. Observer states include Mongolia and Afghanistan, with dialogue partners ranging from Sri Lanka and Turkey to Qatar, Egypt, and Laos. The SCO grouping accounts for around 3.96bn people and $72 trillion in GDP, or 36% of global output.

Accounting for overlaps between the two blocs—such as China, Russia, India, and Iran—the consolidated total is at 5.26bn people and $95 trillion in GDP. With additional countries such as Turkey, Bahrain, or Mexico under consideration for future membership, the bloc’s demographic share could exceed 70% of the world’s population by 2030.

Chinese trade dominates

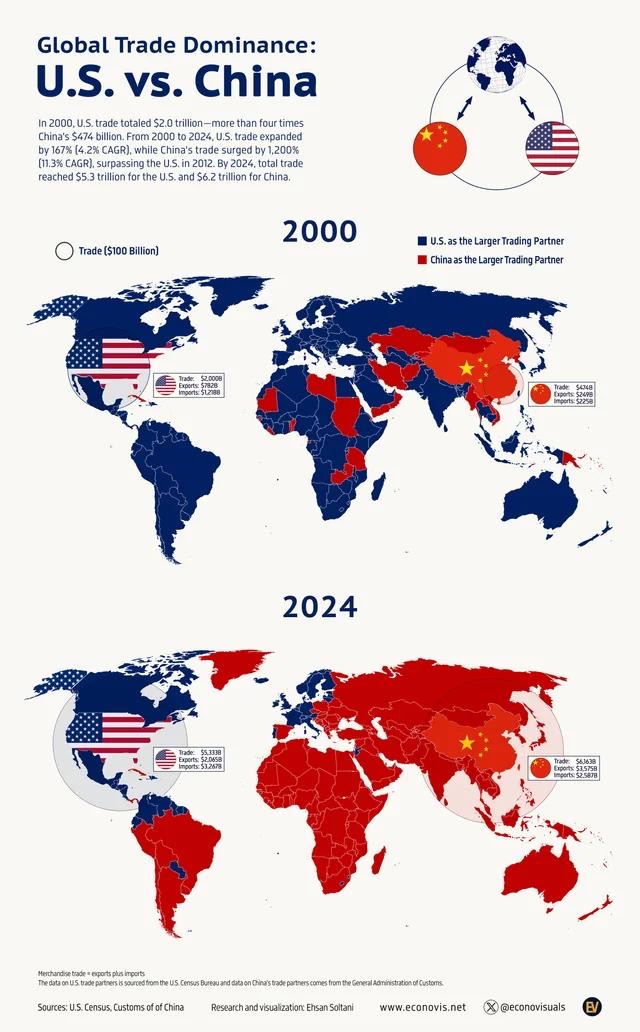

Home to the biggest economy in the world in PPP terms, Chinese trade dominates the group; it has become the biggest trade partner by far with all the countries in Asia, accounting for 80% of the total regional trade, but competing with ASEAN and Japan.

China is also is a major partner with many countries further afield: a top three trade partner for about 120 countries globally in 2025, including the EU ($786bn), US ($688bn), and Africa/Latin America (Brazil: $150bn).

Amongst the BRICS nations, China's 2024 exports were $1.2 trillion versus the total intra-BRICS bloc trade of $500bn, the dominant hub for commodities, tech, and infrastructure. In the SCO, China accounted for 60% of trade flows, largely driven by the Belt and Road Initiative (BRI) investments of over $1 trillion of commitments.

China’s trade dominance, particularly within the BRICS and SCO bloc, stands unrivalled. In 2025, China’s trade surplus is poised to swell to nearly $950bn, with exports of $3.4 trillion dwarfing the $2.5 trillion in imports. This imbalance has fuelled international friction and retaliatory tariffs from the US—ranging from 10% to 27%.

The US is grappling with a $400bn trade deficit with China, while the EU contends with a €200bn shortfall, a gap widening now from the surge in Chinese electric vehicle exports. Even in Asia, surpluses persist—$50bn with ASEAN, for instance—though local manufacturing is beginning to nibble at the edges.

The surpluses are rooted in an export-led growth model, but that has been giving way to a domestic consumption model for several years already. China mitigates tensions with partners by recycling surpluses into BRI geopolitical leverage that promotes their growth.

Several countries have gotten into trouble overextending themselves, borrowing from Beijing for large infrastructure projects. In 2017, Montenegro got into financial straits by overborrowing from China to build the Bar-Boljare motorway connecting Montenegro’s largest port, Bar on the Adriatic coast, to the Serbian border – a BRI project. But in recent years, many of China’s partners have become more cautious, trying to avoid falling into this sort of debt trap. Uzbekistan, for example, is investing heavily into building out its renewable energy sector. However, it has sought to diversify its partners and brought in investors Masdar from the UAE and ACWA from the Kingdom of Saudi Arabia (KSA) which are investing billions of dollars, to diversify away from Chinese help, raising BRI loans from Beijing only as a last resort.

China’s growing economic power and rising trade volumes are starting to impact the economies of the DMs, which is new. Sales of China’s BYD EVs in Europe overtook those of US firm Tesla for the first time ever in April.

China’s growing dominance in global manufacturing exports is intensifying competitive pressures on Central and Eastern Europe (CEE) the European Bank for Reconstruction and Development’s (EBRD) warned, threatening its already moribund competitiveness, the Bank said in its latest Regional Economic Prospects report.

The global manufacturing profile and related trade is changing fast as China moves rapidly up the value-chain. China’s share of world manufacturing exports rose from less than 10% in 2000 to 25% in 2024, according to the World Bank, overtaking the combined exports of the US and Germany. Its export profile has also diversified rapidly, with strong growth in sectors such as EVs where it has become dominant and batteries—industries that are central to the export base of countries including Hungary and Poland. Notably, this year Sweden’s battery-maker Northvolt went bust, unable to compete with cheaper Chinese imports.

Thanks to China’s rapid advances in technology, developing nations are increasingly unable to compete with China, say analysts at Goldman Sachs. Those advances have already made European clean-tech start-ups “uninventable.” Eight venture capitalists flew to China in September to inspect Chinese factories and on their return stripped all European clean-tech investment projects out of their portfolios as they were no longer economically viable. “China is too far ahead. Europe will never be able to catch up,” one of the managers told Bloomberg.

French automaker Renault’s vice-president Jean-André Barbosa recently warned that Europe is no longer a net exporting Weltmeister if automotive exports are stripped out of the statistics during a conference in Brussels.

The Russian sanctions and the end of cheap energy imports has led to the deindustrialisation of Europe. Heavy industry has been decimated and the automotive sector is now in decline. Volkswagen narrowly avoided closing two German plants this year for the first time in its history, but only after it came to a compromise with the IG Metal union that will still see thousands of workers laid off. Porsche has abandoned its EV SUV, unable to compete with Chinese versions. A recent poll found a third of Germany's large businesses are either contemplating relocating to the emerging markets or have already started the process of moving.

Complimentary exports

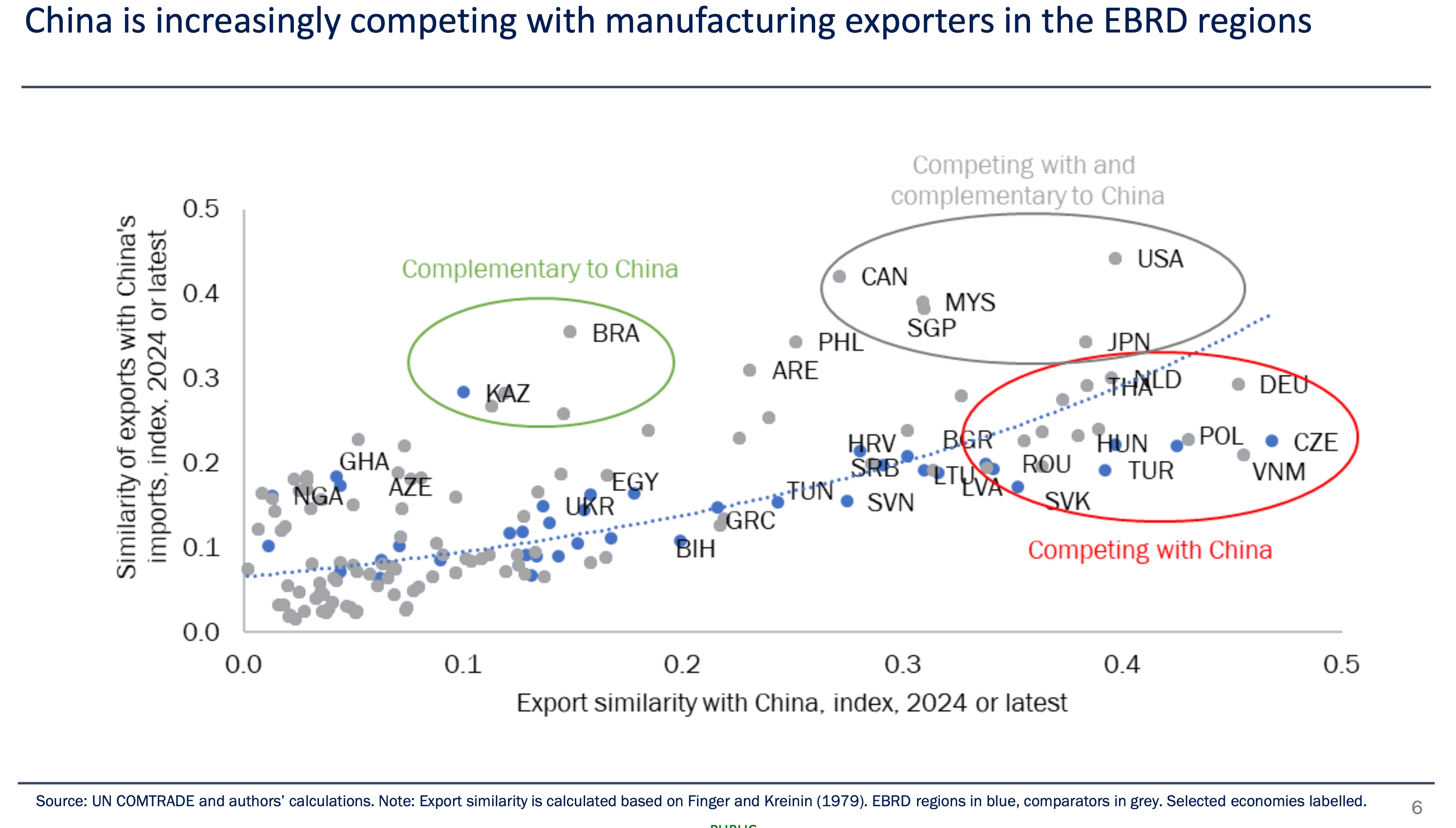

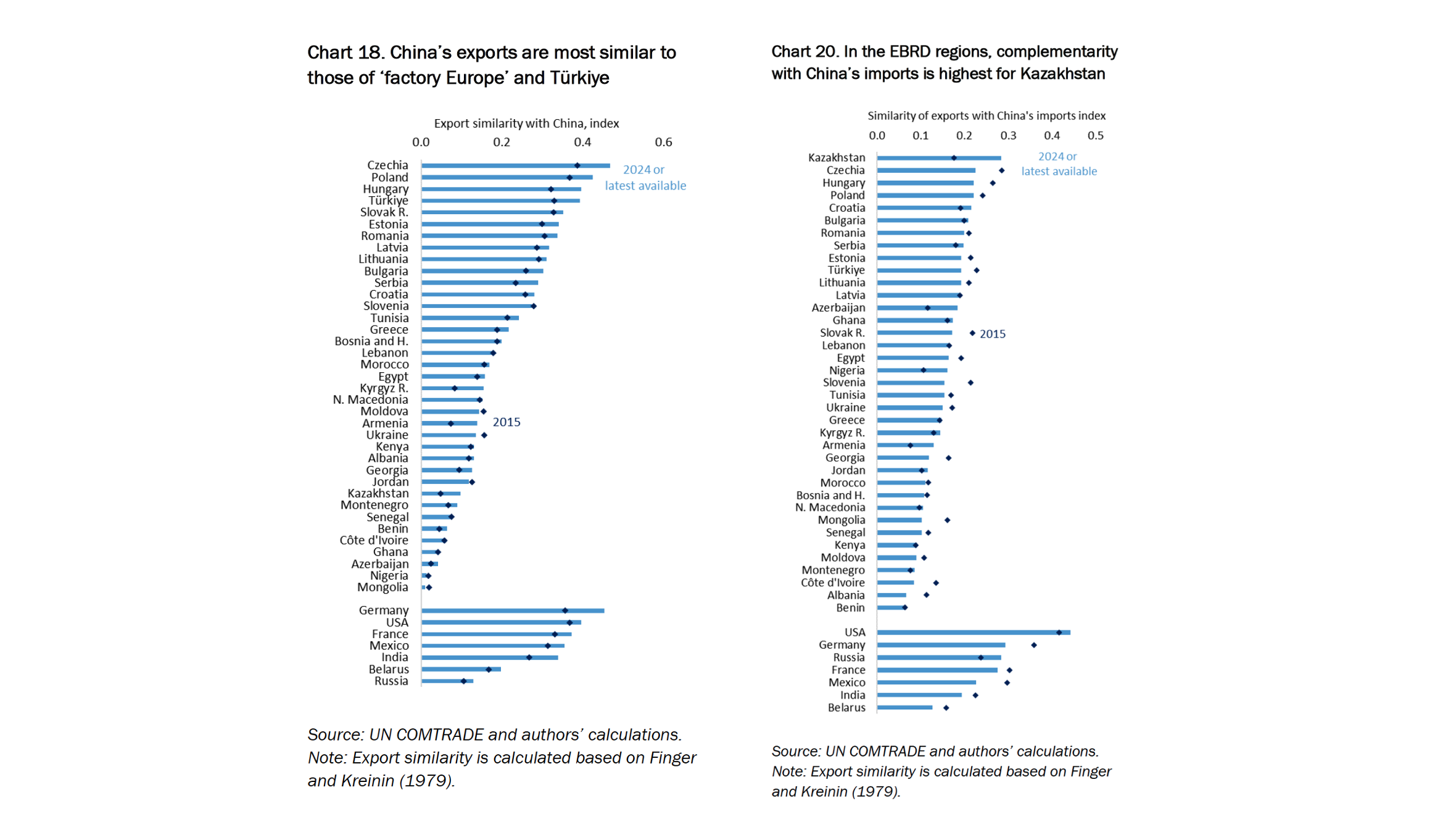

While China’s progress is a problem for developed markets where they compete head-to-head, it has been a boon for many developing markets where Chinese trade is complimentary. The key is if these markets work in overlapping fields where mutual cooperation is beneficial, says the EBRD. In general, the GEMs benefit from cooperation with China, whereas the DMs are finding themselves in stiff and growing head-to-head competition.

“China’s exports have become more ‘similar’ to those of advanced economies and other emerging markets since 2022, with particularly sharp increases observed for economies in the EBRD regions,” the report said.

Using an index of export similarity based on the Finger–Kreinin method -- an index from 0 (no overlap) to 1 (perfect overlap) – the Bank found that China’s export structure is now closest to that of emerging European economies, Kazakhstan and Turkey.

Complementarity with China’s imports vary across regions. The EBRD noted that complementarity is highest for higher-income economies and commodity exporters, including Kazakhstan, Brazil, Malaysia and the Philippines. “Complementarity for commodity exporters has also been rising, while it has been declining for manufacturing exporters,” the EBRD said.

For countries such as Czechia, Hungary, Poland, the Slovak Republic and Turkey, rising export similarity means they increasingly face China as a direct competitor in manufacturing markets. Germany, too, is exposed to this trend, given its high reliance on industrial exports.

The resource-based emerging economies benefit from growing Chinese demand for raw materials. Kazakhstan’s exports, dominated by commodities, are among the most complementary to China’s imports, the EBRD noted. Likewise, Russia and China are a synergy made in heaven.

The Bank added that several advanced economies—including the US, Canada, Japan and Singapore—simultaneously compete with China in export markets while enjoying strong complementarity with Chinese imports, as in addition to manufacturing, they have a large share of commodities in their production mix.

Russia’s special trade relations with China

The trade between Russia and China is a bit special. It has expanded dramatically as Beijing aids Putin's switch from east to west, growing from a modest $107bn in 2020 to an estimated $240bn in 2024, with projections for 2025 hovering around $250bn based on first-half figures of $115bn.

The change is not just due to economic necessity but a strategic pivot toward Beijing to get out from under the Western sanctions as part of the new “no limits” partnership. What began as a complementary partnership—Russia supplying raw materials in exchange for Chinese manufactured goods—has deepened into a near-exclusive lifeline. Trade volumes have surpassed pre-pandemic levels by over 120%.

Central to this boom is Russia's ramped-up energy exports, particularly oil, which now account for nearly 40% of bilateral trade. In 2020, oil shipments to China totalled around 1.6mn barrels per day; by 2024, that figure had climbed to over 2.3mn bpd, often at discounts of $10-20 per barrel below Brent benchmarks. That has earnt Beijing savings of up to $20bn annually.

Russia has also been a winner as food exports to China’s previously closed market, including wheat, soybeans, and meat, surged 150% to $5bn in 2024, filling gaps left by disrupted Ukrainian supplies, with China importing over 7mn tonnes of Russian grain in 2024 alone. The trade is also an important source of yuan earnings for yuanization of the Russian economy after it was forced to dump the dollar due to sanctions. The partners now settle their mutual trade almost exclusively in local currencies as part of their de-dollarisation efforts.

Russia is also increasingly leaning on Chinese equipment and technology to modernise, with machinery and electronics comprising 35% of inflows by 2024, up from 25% in 2020. From Huawei telecom gear to Sany construction cranes, these purchases—totalling $80bn last year—used to largely come from Germany.

But an asymmetry in trade persists: Russia's trade surplus with China narrowed to $50bn in 2024 from $70bn in 2022, as Beijing extracts concessions on pricing and technology transfer. While the partnership has stabilised Russia's finances (trade now covers 60% of its current account deficit), it risks over-dependence, with experts warning of a "vassal economy" dynamic.

In contrast to its booming Sino-Russian trade, Russia's economic ties with the EU have contracted very sharply over the same period – an extreme example of how the changing relationship between the Global North and South are affecting trade.

Total EU-Russia bilateral trade turnover fell from a peak of €257.5bn in 2021 to €67.5bn in 2024, a decline of over 74%, according to Eurostat data. This reflects a 61% drop in EU exports to Russia (from €99bn in 2021 to €31.5bn in 2024) and an 89% plunge in EU imports from Russia (from €158.5bn to €36bn in 2024), driven by energy embargoes and restrictions on goods like machinery and chemicals.

The downward trend began pre-invasion following the 2014 annexation of Crimea, with 2020 turnover being hit by the coronavirus pandemic at approximately €200bn, but accelerated post-2022: €240bn in 2022, €150bn in 2023, and €67.5bn in 2024. By the second quarter of this year, the value hit a 20-year low, with EU imports from Russia at €1.9bn (down from 9.5% share in 2022) and exports rising slightly to €2.4bn, yielding a rare €0.5bn surplus for the EU.