“As Ukraine enters autumn 2025, its economy teeters on the brink of a new macroeconomic shock, with its recovery potential exhausted,” Kyrylo Shevchenko, the former head of the National Bank of Ukraine said in an opinion piece on September 18.

As reported by bne IntelliNews, fears that Ukraine is in danger of a financial crisis have mounted rapidly in recent weeks after the IMF warned that it thought Ukraine would need an addition $10-$20bn of external funding in 2026, on top of currently unfunded $37.5bn the Ministry of Finance (MinFin) has already said it needs to close the budget deficit. Kyiv has approved a draft State Budget for next year that devotes record sums for defence with a projected deficit of 18.4% of GDP – some UAH2.4 trillion (€60bn). That is equivalent to the total amount of money the allies have sent in three years of war - and that is just for the civil spending.

Ukraine spends 31% of its GDP – roughly €107bn a year – on the war, compared with Russia’s €140bn war budget. Kyiv can cover only half of that amount through taxes and domestic borrowing, while the rest falls on the shoulders of its allies. ‘Plan A is to finish the war, Plan B is €107bn,’ Zelenskiy said last wee week

The chance of raising this amount of money from Europe alone is dwindling as Europe can’t afford to take over the burden of supporting Ukraine, as most EU countries are either in recession or approaching a crisis. The problem of funding has escalated since the withdrawal of support by the Trump administration, as under former US President Joe Biden, the US was supplying around 40% of all the funds sent to Kyiv. Since US President Donald Trump took over the US has sent almost no money to Ukraine at all, placing the entire burden on Brussels at a time when several of the leading economies are already facing financial crises of their own.

Russia is also facing economic problems and recently they are getting worse, but Ukraine’s funding needs are much larger; Russia has been able to pay for the war with its continued commodity exports, but Ukraine depends on external funding from allies for half of its deficit for around $50bn a year. If military aid is included then the cost of the war is running at an estimated $100bn a year is running at between $100bn to $150bn a year, according to Timothy Ash, the senior sovereign strategist at BlueBay Asset Management in London.

“The low-base effect from 2022, which drove record GDP growth in Q2 2023 (+19.5% y/y), has fully dissipated. Economic momentum began to slow by late 2023, and by Q4 2024, the economy had slipped into recession (–0.1% y/y),” Shevchenko, who goes on to describe Ukraine’s deteriorating economic outlook. “Stagflation has become the new norm. The GDP deflator in Q1 2025 reached 16.9%,” he said, adding: “Public debt has hit 100% of GDP (≈$185bn), with $139bn external and $46bn domestic.”

Ukraine went into the war in a relatively healthy state and was closely supervised by an IMF Extended Fund Facility (EFF) programme. In 2021, real GDP growth was 3.4%, reaching nearly $200bn in current prices.

But the shock of the Russian invasion was immediate: GDP contracted by 29.1% in 2022, as Russia cut off Ukraine’s access to the sea, bottling up grain exports that are the country’s biggest earner of foreign exchange. The ports handled 70% of grain exports and immediately came to a near standstill. At the same time over 6mn people fled the country, gutting the workforce.

In the last two years Ukrainian President Volodymyr Zelenskiy has increasingly put the economy on a war footing; earlier this month he said that Ukraine is now producing around 60% of all the arms and ammo it needs.

But now the rebound is fading. “2023: GDP growth reached +5.3%… 2024: Growth slowed to +4.1%, signalling the exhaustion of post-shock recovery momentum,” says Shevchenko. “Structural weaknesses persist. Exports rely heavily on agriculture… Fixed capital investment remains critically low at 6–7% of GDP, compared to the 15% needed for sustainable growth… Approximately 55% of the state budget is financed by foreign donors.”

The outlook for this year is of slowing growth as the economy bumps up against these structural limitations. Growth in the first quarter is already down to 0.9% and fell further to a “statistical error” of 0.6% in the second, says Shevchenko. The forecast for the rest of the year is the economy will start to contract in the third and fourth quarters, says Shevchenko.

“Industry is in steady decline (–5% y/y),” while “exports are weak (–5% y/y)… grain exports (–24%, or –$3.5bn)… imports of electrical equipment surged by +68% (+$4.4bn), highlighting domestic industry’s inability to meet energy and defence needs,” says Shevchenko.

Most of the attention has been on the foreign investment into the defence sector and external funding for the budget deficit, but Ukraine’s balance of payment situation has been deteriorating over the last two years. As bne IntelliNews reported, Ukraine runs a $20bn trade deficit with Europe. That was made worse after Poland unilaterally cut off Ukraine grain imports after cheap Ukrainian grain wrecked the Polish grain market that year and those bans remain in place. That was made worse after the Deep and Comprehensive Free Trade Areas (DCFTA) duties and quotas exemptions expired on July 5 further limiting Ukraine’s exports to the EU and costing Ukrainian producers hundreds of millions of euros in charges.

“In July 2025, the trade deficit hit a record –$4.37b. For January–July 2025 the trade balance was a negative $24.52bn, according to Shevchenko.

That negative trade balance is starting to eat into the country’s international reserves which were a record $43.03bn as of August 1 and still a healthy 4.7 months of import coverage. But Shevchenko warns that without more external aid the reserves will start to fall. “Without external aid and interventions, the currency market would collapse within a quarter,” he said.

“Western financial support is no longer sufficient,” Shevchenko argues. “The latest EU tranche of €4bn was cut by €1.5bn. Total aid under the Ukraine Facility since March 2024 amounts to €22.7bn, but the 2026 budget assumes ongoing conflict, cementing fiscal dependence.” MinFin has said there is already an $8bn-$19bn shortfall for this year’s budget. (The spread depends on if a ceasefire is called or not).

Shevchenko recommends dramatic action to face up to the realities of the situation and the fading support as Ukraine’s international partners struggle to find more cash.

- Float the Exchange Rate: A devaluation shock would curb imports, boost exports, and preserve reserves.

- Launch Long-Term Refinancing Operations (LTRO): 5–7-year programs with state guarantees to revive business lending.

- Increase Capital Investment: Raise spending on energy, transport, and industry to 2–3% of GDP.

- Prepare Debt Restructuring (LMO-2): Act proactively to avoid a crisis in 2026–2027.

“However, implementing these measures requires political will, which is currently lacking. Ukraine is thus balancing on the edge of a macroeconomic collapse,” says Shevchenko.

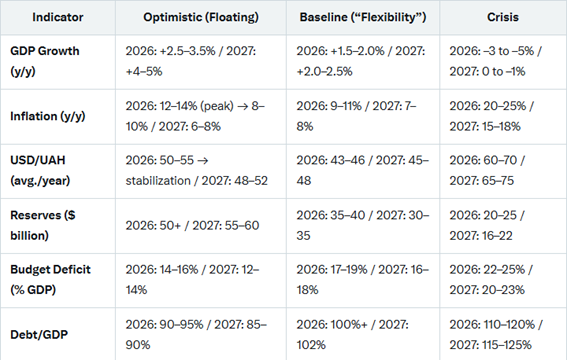

Macroeconomic Indicators by Scenario: