_1781191847.jpg)

Why the Baku-Supsa pipeline is back at the center of the energy game

15 hours ago

Politics

The scale of the early June countrywide demonstrations seen during the snap election to replace ruler of three decades, 79-year-old Nursultan Nazarbayev, with his handpicked shoo-in successor Kassym-Zhomart Tokayev took many observers and the authorities by surprise. Ever since, protests in Kazakhstan have hit the headlines almost every week, albeit they have been at a much smaller scale. To mild astonishment, the government appears to have taken the hint. Aside from announcing social spending programmes to tackle economic inequalities—often seen as key drivers behind political protests—Tokayev announced in December a reform package that will drop a requirement that public protests need approval from the authorities. Moreover, the reforms also promise to make it easier to form political parties and reduce punishments for hate speech and libel. The year of 2020 will show whether Tokayev’s promises are merely just that—promises.

Tokayev’s decision-making is hampered by Nazarbayev. Behind the scenes, he continues to wield influence via the influential National Security Council and his constitutionally-approved special status as “Yelbasy” (“Leader of the Nation”). Since October, Tokayev has been required to confirm the appointments of all but three ministers with Nazarbayev, though even the exceptions (the ministers of defence, interior and foreign affairs) had to be discussed by the Security Council. The same approval process applies to provincial governors and some other senior officials, such as the chief of KGB successor, the Committee for National Security (KNB).

The regulation of Tokayev’s freedom to appoint allies might have come around after he managed to anger a few of Nazarbayev’s allies within the Kazakh elite. A report by opposition-oriented analytical website Kazakhstan 2.0: The Expert Communication Channel for the Central Asian Region pushed the theory that Tokayev broke unspoken rules of respect for Nazarbayev’s oligarch son-in-law Timur Kulibayev during his September visit to the city of Atyrau by the Caspian Sea. The visit was officially meant to be part of a 120-year anniversary celebration of Kazakhstan’s oil and gas sector. But it supposedly sidelined Kulibayev, who has long stood as a “key player” in Kazakhstan’s oil and gas industries, partly thanks to his status as head of an important energy lobby group, Kazenergy. Kulibayev, who is married to Nazarbayev’s daughter Dinara Kulibayeva, also heads the Atameken National Chamber of Entrepreneurs and formerly chaired the Samruk-Kazyna sovereign wealth fund.

Tokayev’s treatment of Kulibayev at the event is held by some observers to be part of a larger squabble for influence over Kazakh business and politics. Kulibayev is not the only member of Nazarbayev’s inner circle that the current regime disapproves of. Allegedly another close ally of Nazarbayev, billionaire Bulat Utemuratov, is also on shaky ground.

These inter-elite conflicts are likely to continue in 2020 but are unlikely to have any major impact on Kazakhstan’s power structure, excluding the scenario of Nazarbayev passing away.

The authorities are expected to continue tackling the issue of ongoing anti-China sentiments among Kazakhs throughout the country. In 2019, they produced some violent demonstrations, with protesters pushing the line that China is economically an invasive force. Anti-China sentiments were exacerbated in 2019 by constant news of China’s “re-education camps” in Xinjiang, said to hold masses of detainees including thousands of ethnic-Kazakh citizens of China. As a result, the frequency of protests directed at China and its investments in Kazakhstan intensified, although the demonstrations were meagre compared to the land reform protests of 2016 that spanned the entire country.

At the end of the day, the anger at China is more of a symptom of economic dismay among Kazakhs rather than an expression of pure concern at the impact of the Chinese. If Tokayev’s social spending programmes produce quality-of-life improvements, it will be interesting to see whether that will be sufficient to keep Kazakhs away from organising around this anger.

Macroeconomic

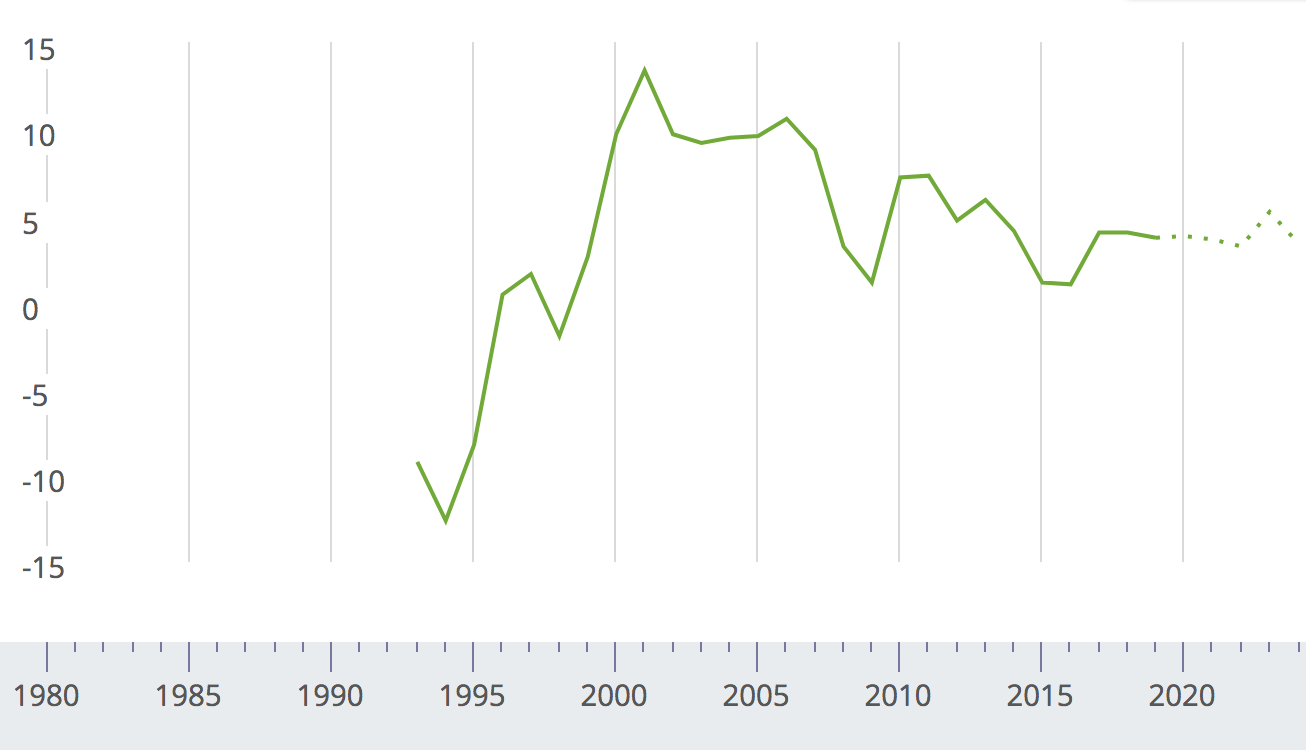

The trajectory of Kazakhstan’s growth in 2019 appeared to contradict projections made by analysts who expected a slight slowdown by the end of the year. Kazakh Prime Minister Ruslan Davlenov announced a January-October GDP expansion of 4.4%, surpassing the 4%-4.1% fluctuations recorded throughout 2018 and the first half of 2019.

In contrast, the World Bank forecast that Kazakhstan’s growth would slow to 3.9% in 2019 on the back of sluggish demand and stagnant oil production. It fell 0.5% y/y in the first nine months of this year. Oil output started growing again after a boost in October, recording a 0.5% y/y rise in January-October. But that alone does not explain the improvements in the economic growth of Central Asia’s biggest economy.

Much of Kazakhstan’s latest growth appears to have been driven by non-oil growth, including an expansion in the services sector and construction projects. Construction has been substantially supported by China’s Belt and Road Initiative—construction works in infrastructure to support China’s growing trade with Europe has been a priority in the past couple of years. A recovery in consumption and continuing investment activity have stood as key drivers of growth in Kazakhstan thanks in part to the government’s fiscal support and to a rise in retail lending. The International Monetary Fund (IMF) has said it expects non-oil growth to stay strong in the near future. The Fund still expects a slight slowdown in growth from the past two years, however.

The IMF projects Kazakhstan’s growth at 3.8% in 2019, in the absence of significant shocks, and at a slightly higher rate in 2020 thanks to the recovery in the oil sector. Risks to the IMF’s outlook stem from fluctuating commodity prices along with geopolitical and trade tensions involving major trading partners.

The Russia-led Eurasian Development Bank (EDB) and Kazakhstan’s own central bank expect GDP growth at 4.2% in 2019 and both see it slowing in 2020, falling to 3.5% and 3.8%, respectively.

Kazakhstan, GDP growth. Source: World Economic Outlook, IMF.

According to the central bank, Kazakhstan’s current account payment balance had a $1.9bn deficit in the first half of 2019. It forecasts that the current account deficit will stand at 2.2% of GDP in 2019 and 3.1% in 2020.

External debt amounted to $158.3bn, or 87.7% of GDP, in the first half of 2019—the figure was below the $164.4bn (96% of GDP) recorded in the same period of 2018. Much of Kazakhstan’s debt in the past couple of years has been driven by the aforementioned investments by China, amid attempts to move away from economic dependence on oil exports and efforts at building business in the transit of Chinese goods and boosting food and agricultural exports to China and elsewhere, among other non-oil activities.

The volume of cargo transportation by rail between Kazakhstan and China grew by 23.8% y/y to 14.2mn tonnes in the first 10 months of 2019. State-run railway operator Kazakhstan Temir Zholy (KTZ) has said that the volume of cargo may reach 16.5mn tonnes by end-2019, exceeding the planned volume of 15mn tonnes and last year’s volume of 14mn tonnes.

Overall, Kazakhstan’s trade balance stood at a surplus of $1.286bn as of October, down from a surplus of $1.8bn recorded in October 2018. The shrinking trade surplus was mainly a result of a boost in imports of equipment and machinery for modernising Kazakhstan's oil refineries and the carrying out of infrastructure projects, among other things. A similar direction can be expected for 2020.

The Kazakh national currency, the tenge, which traded at KZT381.8 against the greenback on January 1, 2020, is expected to continue to weaken this year amid volatile oil prices. In the near future, the tenge is likely to continue to trade with the upper threshold of KZT387 to the dollar.

Kazakhstan’s total government spending for 2020 has been set at KZT12.9tn.

Inflation and rates

Kazakhstan’s central bank kept its policy rate unchanged at 9.25% on December 9, but warned that inflation may pick up in the first quarter of 2020—the next policy rate review is set for February 3.

The regulator cut its policy rate to 9.25% from 9% on September 9. It cited increasing inflationary pressures as the primary reason behind the rate hike. The national lender previously warned it might increase the rate if it saw greater risks to its inflation target. The regulator identified increased domestic spending and expectations of a global economic slowdown as among the key risks to its targeted inflation rate. Further policy decisions would depend on consumer price dynamics, import growth, domestic demand and global economic conditions, it said.

Going further back, the National Bank of Kazakhstan (NBK) cut the policy rate by 0.25 pp to 9% on April 15. Following that move, annual inflation rose to 5.4% by June, from 4.9% recorded in April, reversing its course from the previously recorded descent. Inflation also registered at 5.4% in November, down from 5.5% in October. Experts have partly attributed the rise in inflation to increased social spending by the government.

An IMF mission statement in November forecast inflation will remain elevated next year “as the effect of utility price cuts in 2018 dissipates”.

The central bank has previously said that it expects inflation to stay at between 4-6%. It said on December 9 that inflation may accelerate to the upper boundary of the target inflation corridor in the first quarter of 2020 due to rising tariffs on services and growing food prices.

Business regulation

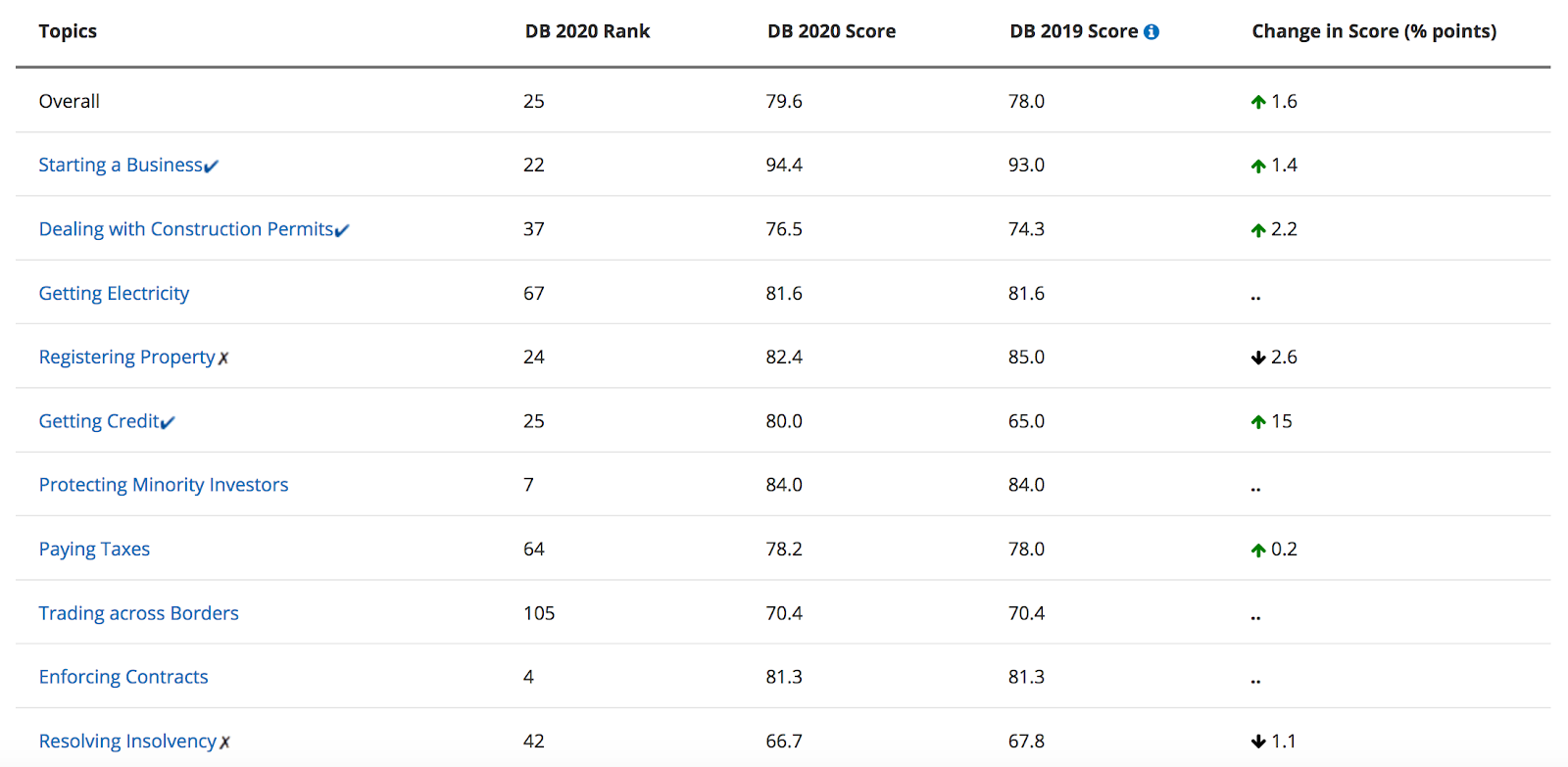

Business regulation changes in Kazakhstan have improved the ease of doing business over the past two years, the World Bank said in its Doing Business 2019 report released in June. Kazakhstan saw its global ranking improve to 25th position from 28th last year among the 190 ranked economies. It registered a score of 79.6 compared to last year's 78.

Kazakhstan Doing Business Scores & Rankings, Source: Doing Business Database, World Bank.

Most significant regulatory progress was recorded in the Kazakh capital, Nur-Sultan. The report measured four regulatory areas: starting a business, dealing with construction permits, getting electricity, and registering property.

Across the areas measured, Almaty achieved the highest score by leading in getting electricity, registering property and dealing with construction permits. Nur-Sultan ranked first for starting a business, thanks to the availability of electronic processes and the usage of the e-government system. East Kazakhstan and Pavlodar shared top scores with Almaty for registering property.

The World Bank noted that Kazakhstan had experienced a fast pace of reform across the country with lower performing regions closing the gap on top performer Almaty in getting electricity and dealing with construction permits. The reforms were reducing red tape for entrepreneurs as well as leading the nation towards global good practices in business regulation.

“As Kazakhstan strives to improve opportunities for all citizens and diversify its economy through increasing the contribution of small and medium-size enterprises, the right regulatory environment can help entrepreneurs overcome obstacles such as low productivity and corruption. Better managing the pace of reforms and addressing gaps in implementation will enable firms to realize their full potential and contribute to growth,” said Ato Brown, World Bank country manager for Kazakhstan.

Oil and gas

Kazakhstan’s oil production stood at 82.5mn tonnes in January-November, where around 60% of the nation’s oil output came from the huge Tengiz, Karachaganak and Kashagan oil fields.

Hydrocarbon-export-reliant Kazakhstan has seen much of its oil output boosted by the giant Kashagan oilfield in the Caspian Sea. This year, Kazakhstan performed maintenance works at the field, temporarily bringing down overall oil output, but now the oil production figures are recovering.

The country is aiming to produce around 89mn-90.5mn tonnes of oil in 2019 with the long-term goal of staying at an average level of 90mn tonnes in the next 2-3 years.

Oil exports registered at 65.791mn tonnes of oil in January-November, 0.4% below last year’s level for the same period. The goal for 2019 is to export 70.5mn tonnes of oil. A boost in oil exports next year may arise from Kazakhstan’s plans to sign an agreement in 2020 to supply 1mn-3.5mn tonnes of oil along with oil products to Belarus. The suggestion to import Kazakh oil was originally made by Belarus in the wake of Russia halting oil flows via the Druzhba pipeline in April after contaminated oil was discovered.

Kazakhstan’s own domestic consumption of hydrocarbons is set to continue growing, especially given the completion of work on the $700mn Saryarka gas pipeline. KazMunayGas (KMG) announced in October that works on the pipeline were wrapped up, but the announcement was only in reference to the welding of the pipeline—the remaining segments of the project, including branch pipelines, gas distribution stations and measuring stations were due to finish up by December 31.

Modernisation works at all Kazakh refineries were finalised earlier in 2019. The energy ministry set plans to process 16.2 tonnes of crude oil in 2019 at the three newly upgraded refineries and produce approximately 4mn tonnes of diesel fuel and petrol during the year, respectively. The amounts are said to be more than sufficient for meeting Kazakhstan's domestic demand for fuel. Kazakhstan used to rely on imports of fuel from Russia.

Agriculture

The agriculture sector has been a priority area for development in the past two years, with weak oil prices forcing Kazakhstan to diversify its economy away from hydrocarbons.

This year, multiple projects in the sector were adopted with the purpose of attracting foreign investment. The latest include an agreement between US-based Valmont Industries, the Kazakh Ministry of Agriculture and Singapore-based Kusto Group signed on the principles of effective irrigation and improving agricultural productivity in Kazakhstan. The document envisages the construction of a plant for the production of Valley Pivot Irrigation Machines in Kazakhstan in 2022. The US irrigation technologies are set to increase crop productivity and reduce agricultural costs by 50%. Kazakhstan is planning to increase the area of its irrigated land from 1.4mn to 2mn hectares by 2022 and to 3mn hectares by 2030.

Grain, a major segment of the sector, saw a 2019 harvest of 19.1mn tonnes, 9.5% below 2018’s year’s yield. The decline was driven by a hot and arid summer season. In addition to abnormal summer heat, Kazakhstan saw prolonged precipitation of 15-20 days that affected both the grain quality and its yield. As a result, Kazakhstan expects a 3mn-tonne fall in its grain export potential during the 2019/2020 marketing year.

During the autumn season, Kazakhstan’s state-run grain exporter Astyk Trans announced it was launching a “pilot regime” to reduce tariffs on exporting grain to Iran, Afghanistan and China, cutting the tariffs to 30% from 35%. The measure is aimed at supporting domestic grain exporters. If it ends up leading to an increase in overall grain exports, the measure would become permanent, according to Astyk Trans.

The government has been sticking to its pledge to pump KZT423bn (€1.2bn) into the country's grain industry during 2017-2021 as part of a programme to improve industry profitability by 30%-40%. That includes ongoing efforts to shift exports toward oilseeds and pulses away from wheat.

Kazakh beef production and cattle farming are seen as a growing subsector of agriculture with expectations that beef and cattle exports will double in 2019 thanks to higher global prices against the backdrop of a severe protein shortage in neighbouring China and growing demand for meat products in Central Asian neighbour Uzbekistan. The agriculture ministry has been discussing the possibility of temporarily banning exports of livestock to encourage the processing of meat domestically and in order to build up the exporting of processed products.

Banks

A review by an IMF team in November commented on the state of the Kazakh banking sector, noting that the recently competed asset-quality review (AQR) of the 14 largest Kazakh banks would be instrumental in fully understanding the health of bank operations and balance sheets and identifying required actions.

“The AQR was launched by the NBK in mid-2019, with results expected early next year,” the IMF said. “Based on the AQR findings, the authorities will formulate follow-up actions, which may include bank recapitalization by existing or new shareholders. State support, if any, should go only to large and viable banks subject to shareholder contributions and the adoption of comprehensive restructuring plans. In the team’s view, state support should not come from the NBK.”

Despite state support, the banking sector remains weak, plagued by high levels of bad loans. The Fund views the authorities’ plan to conduct an external asset quality review (AQR) of medium sized and large banks as “commendable” and believes it should set the basis for the long-awaited strengthening of the sector.

The results of the AQR were announced on December 30, revealing that the 14 largest banks were in need of a KZT450bn ($1.05bn) increase in their capital requirements. A report by Reuters, citing anonymous sources, earlier in the month suggested Kazakh authorities planned to provide over $1bn in aid to at least four local banks after holes in their balance sheets were revealed by the asset-quality review. The names of the four troubled banks were not mentioned in the report.

Fitch Ratings said in a note on July 31 that Kazakh banks' bad loans under IFRS 9 were “mostly well above their impaired loans under regulatory accounting” and at some medium sized banks were so large relative to loss absorption capacity that these lenders may need fresh capital injections or other external support. Fitch’s conclusions came after Kazakh authorities announced that there would be no more banking sector bailouts, following banking sector cleanups which started in 2017 and continued into this year, costing Kazakhstan over $13bn.

Fitch said it believed off-government balance sheet transactions, such as through the National Fund, could be used again to provide further government bank support if it were needed. However, the agency saw such state support as highly uncertain. This is reflected in Fitch’s “support rating floors of 'B-' for Fitch-rated medium-sized banks”. If the bailout happens to be carried out by the central bank, it will put pressure on the national currency.

Funding and finance

The Ministry of Finance in September issued euro-denominated bonds in excess of €1,150mn—the issuance was made in two tranches at a nominal cost of €500bn with a 7-year circulation period (at a coupon rate of 0.6%) and €650mn with a 15-year circulation period (at a coupon rate of 1.5%). The issuance came as the costs of eurobonds borrowing stood at a record low in Kazakhstan and other countries of the CIS region. The transaction marked Kazakhstan’s second ever euro-denominated bond issuance, with the nation seeking to diversify its investor base via euro-oriented investors.

Kazakhstan sovereign wealth fund Samruk-Kazyna in the same month sold 9.86mn global depositary receipts (GDRs) representing interests in ordinary shares in Kazatomprom, the world’s largest producer of natural uranium, at a sale price of $13 with gross proceeds of $128.2mn.

Kazakhstan’s sovereign credit rating from Moody’s stands at ‘Baa3’ with a positive outlook, while S&P affirmed its rating this year at ‘BBB-’. Meanwhile, Fitch affirmed its rating at ‘BBB’ in September with a stable outlook.

Kazakhstan is planning to issue a tenge bond equivalent to $1.5bn next year. It will qualify for JPMorgan’s local-currency debt index.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now