BOFIT: Russia faces increasing challenges in balancing its economic policies

1 day ago

The removal of Nicolás Maduro from power by the United States has upended Venezuela’s political landscape — but it is unlikely to translate into a broad-based economic recovery, according to a note by Tim Hunter, Senior Latin America Economist at Oxford Economics.

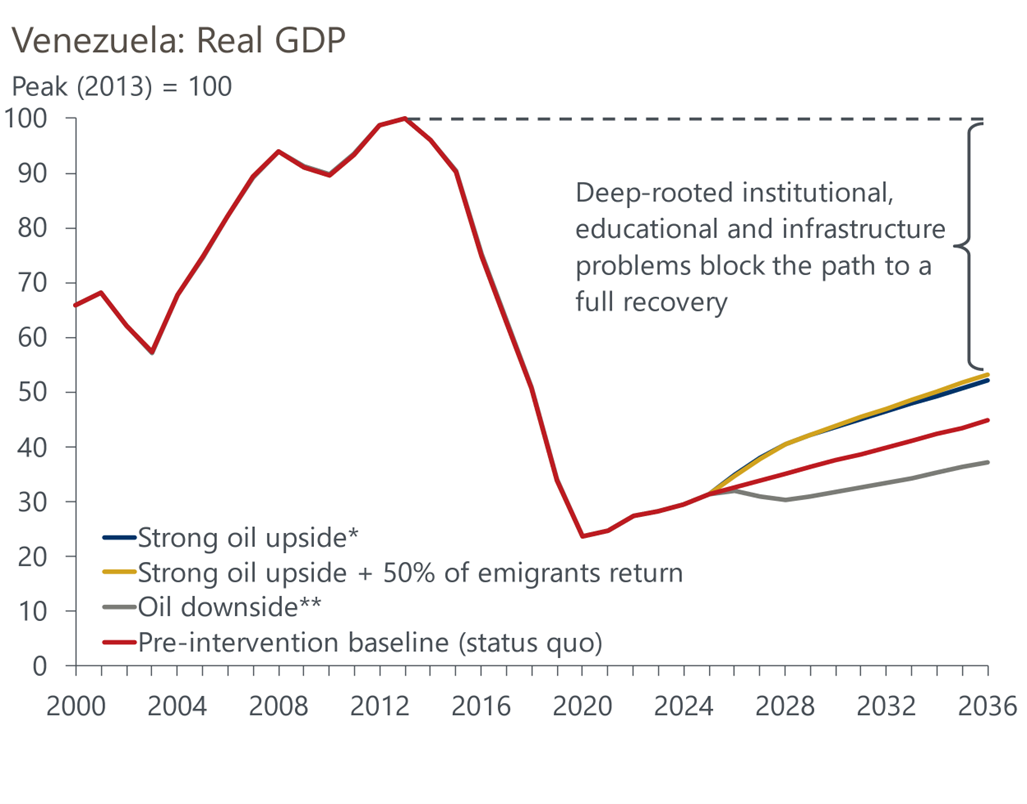

“The scale of the challenges ahead is vast. We estimate GDP in 2025 was almost 70% below its 2013 peak. Under our simulations using our Global Economic Model, even a strong oil upside and 50% of emigrants returning leaves GDP 50% below the 2013 level in ten years' time,” says Hunter. “Widespread improvements to the country's institutions, education, and infrastructure are needed for a more complete economic recovery, alongside a stable security and political environment.”

In the short term, oil output is actually likely to fall further following Operation Maduro on January 3 as the US blockade has limited diluent imports needed to process the country's heavy oil blend and stopped some export tankers from reaching the country, says Hunter.

“This will clip our previous 4.2% y/y 2026 GDP growth forecast. Inflation, which we forecast to peak at almost 600% y/y this quarter, could rise even further if the government increases monetary financing in response to weaker oil revenues,” he added.

Oil export boost

Hunter said that in the near term, modest gains are possible if the US lifts sanctions and allows a cooperative Chavista-led government to remain in power.

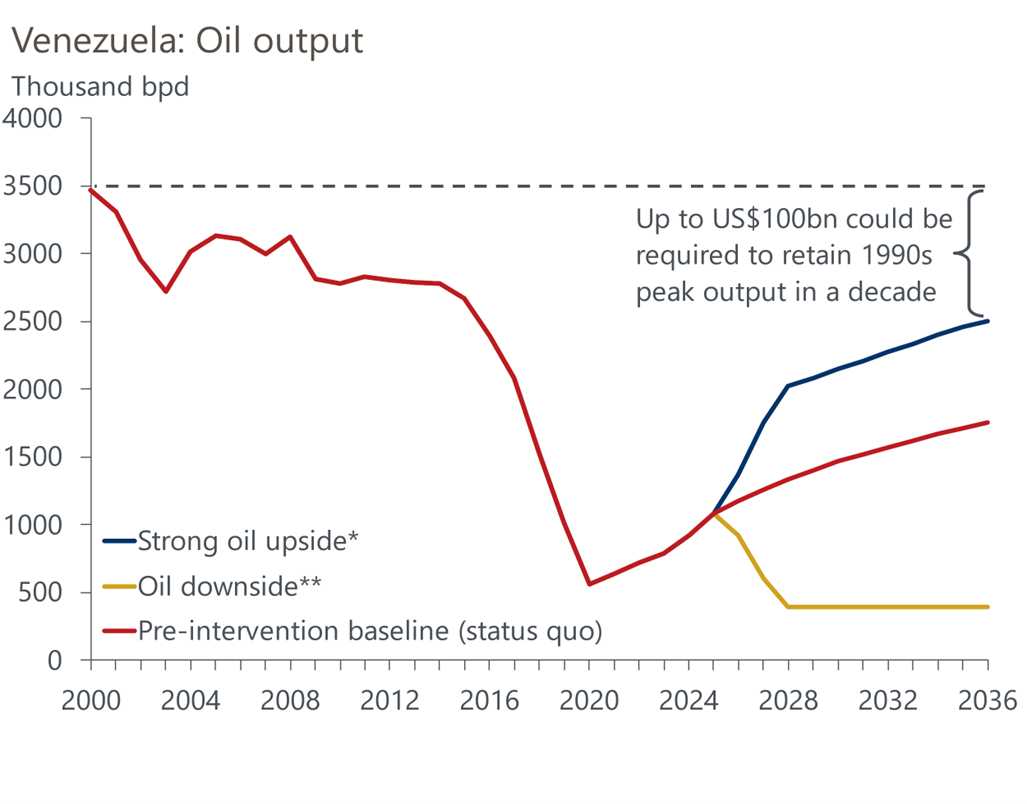

“If sanctions are removed and US firms are allowed back in, oil output could double to 2mn barrels per day by 2028 — but to go beyond that would require at least $15bn–$20bn in new investment, and much more to return to 1990s peak levels.”

In 2025, Venezuela's average oil production was approximately 800,000 to 850,000bpd, down from the 1990s peak of over 3.5mn bpd.

A US-backed economic opening is likely to focus on hydrocarbons, where Venezuela still holds the world’s largest proven oil reserves of an estimated 303bn barrels in the Orinoco Belt. But as bne IntelliNews reported the oil is extremely sour with a very high sulphur and toxic metal content and the country’s refining and transport infrastructure is in tatters. Even if multinational oil companies were willing to ignore the large political risks, they would have to invest tens of billions in modernising the sector that would take a decade to complete. In a recent report, The Economist estimated the cost of modernisation would be an extraordinary $110bn, although other estimates put the number at a still considerable fifth to a tenth of that.

“Hydrocarbons remain the centrepiece,” Hunter noted. “Even at current output of around 1mn bpd, oil still accounts for 10% of GDP. But the sector is badly degraded, and infrastructure for heavy crude is lacking.”

Domestic security and democracy

US intervention has so far stopped short of removing the entire Venezuelan government, with Vice President Delcy Rodríguez acting as interim president. Hunter argued this reflected Washington’s desire for a controllable transition. “A stable, US-loyal government aligns with US objectives: increasing oil production, stemming drug flows, and encouraging migrant return. But it’s not necessarily aligned with Venezuela’s long-term economic recovery.”

Domestic security will be a key determinant. The Venezuelan military remains closely tied to the ruling party. “The armed forces are deeply embedded in the state and economy. Their support is critical. A breakdown in loyalty could lead to instability, with militias or guerrilla forces threatening security — a risk that would deter any meaningful investment.”

Hunter said that while a democratic transition would be desirable, it is not essential for short-term economic gains. “Higher oil revenues can deliver GDP growth without democracy, but long-term recovery will require democratic legitimacy, anti-corruption reforms, and improved policymaking. These goals clash with the interests of the entrenched security elite.”

After decades of governmental mismanagement, holding open elections could increase the chaos and prevent the country from finding a stable political footing, with power flipping between competing factions. That would stymie investment in the hydrocarbon sector and other industries due to a poor investment climate. In this case most migrants would stay away as widespread corruption and poor policymaking continues.

However, following comments by Secretary of State Marco Rubio in the last days, the US is likely to allow the current Rodrigues government to stay in power if it follows the US directives as a short cut to minimising the political instability. Rubio walked Trump’s “we will run Venezuela” comments back, but explicitly threatened more military strikes and sanctions if, “we don’t like what we see happening.”

Hunter says the best-case upside sees an international effort to rebuild the Venezuelan state, generating a broad-based economic recovery alongside the return of most migrants and the introduction of open and fair elections.

However, the downside is if the current Chavista government remains in power and continues its authoritarian rule, “the hollowing out of institutions and policymaking capabilities may prove too severe to recover from,” says Hunter.

Despite the uncertain outlook, one near-term scenario is likely: “We expect modest economic improvements in the next one to two years under a US-backed Chavista government that opens up hydrocarbon investment and maintains domestic order. Some migrants may return. But broader recovery will be constrained, as the current government — and especially the military — is unlikely to allow the reforms needed for lasting change.”

Drawing a comparison with past US interventions, Hunter pointed to Panama’s post-1989 recovery as an ideal — but unlikely — model. “Panama’s GDP per capita has tripled since the US invasion. But Venezuela’s starting point is far worse. The state is hollowed out, and institutions are broken. That makes the road ahead far more difficult.”

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now