.png)

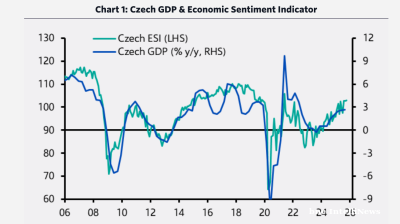

Czech growth accelerates as domestic demand-side pressure builds

1 day ago

The board of the Central Bank of Russia (CBR) has resolved to cut the key interest rate by 200 basis points (bp) from 20% to 18%, as strong disinflation trend in July untied the regulator’s hand in supporting the economy that slides from overheating to recession.

As followed closely by bne IntelliNews, the decision was largely expected by the market, with consensus forecasts unanimously betting on a key rate cut. The majority of the analysts guided for a decisive policy action of at least 200bp rate cut.

Most respondents cited rapidly moderating inflation, resilient ruble strength and slowing GDP growth as key arguments for a deeper rate cut. CBR Governor Elvira Nabiullina had also recently indicated a willingness to cut rates more aggressively if disinflation and economic cooling accelerated.

The banking sector also expected the key rate to be cut, as prior to the CBR board meeting, major banks such as state-controlled Sberbank pre-emptively reduced deposit rates by 1.5 – 2.5 percentage points.

Latest indicators such as deteriorating business sentiment, consumer demand running out of steam, manufacturing PMI index and industrial output data indeed confirmed that Russian economic growth appears to be rapidly slowing down.

As a reminder, the CBR’s June previous key interest rate cut from 21% to 20% was its first monetary easing move in nearly three years. But as inflation finally converges to CBR target, the regulator finally has the space to manoeuvre with its monetary policy.

Inflation in annual terms since been stable in single digits since May. Inflation dynamics withstood utility tariff hike in the beginning of July. Last week the CBR acknowledged that inflation is within its official target for the first time this year.

“The current inflationary pressure, including persistent components, is declining faster than previously projected,” the CBR said, adding that the effects of monetary tightening are becoming more visible, especially in non-food goods.

Despite this disinflationary trend, as followed by bne IntelliNews, inflation expectations remain stubborn.

The CBR indeed noted that “a stable trend towards lower inflation expectations has not yet formed”. At the same time, the regulator confirmed that labour market tensions are easing, with fewer firms reporting staff shortages and wage growth slowing, although still outpacing productivity gains.

The regulator asserts that “given the ongoing monetary policy, annual inflation will decline to 6%-7% in 2025, return to 4% [official target] in 2026, and remain at target thereafter”.

As followed closely by bne IntelliNews, the signs of a slowdown in Russia are clear, with analysts guessing whether the economy overheated by the full-scale military invasion of Ukraine is headed for a “soft” or “hard” landing.

Whether the Russian economy is headed for a recession and the exhaustion of its growth drivers is now a part of policy debate.

The CBR also acknowledged that “the deviation of the Russian economy above the balanced growth path is narrowing”, meaning that overheating is over.

“Real-time data, including for 2Q25, and survey indicators suggest a further slowdown in domestic demand growth alongside continued moderate overall economic activity,” the CBR press release reads.

Previously the analysts expected the key interest rate to be cut to 14%-16% by the end of 2025. This outlook was confirmed by the analysts surveyed by RBC after the 200bp rate cut.

While the CBR’s revised medium-term rate forecast indeed implies a possible cut to as low as 14% by end-2025, the regulator refrained from giving a clear dovish guidance on the monetary policy, stating that “pro-inflationary risks outweigh disinflationary ones over the medium term”.

“The regulator refrained from substantially softening its rhetoric, likely due to concerns over the risks of premature monetary easing. We continue to expect the rate-cutting cycle to persist – reaching 15% by end-2025 and 12% in 2Q26,” Renaissance Capital analysts commented.

Notably, RenCap analysts note that in the press release, the regulator chose not to make any commitments about future rate cuts.

“While further easing is implicitly expected, the lack of a direct signal suggests a deliberate decision not to commit to a firm stance for the upcoming meetings,” RenCap analysts note.

The inflation forecast for end-2025 was reduced by 1pp (from 7%–8% to 6%–7%), which RenCap analysts consider the only clear “dovish” element in the communication. The analysts also see the following press conference of CBR Governor Elvira Nabiullina as neutral in tone.

“Among the changes in the press release, we note the return of geopolitical tensions to the risk list as a factor of overall uncertainty. We see this as a timely reminder to markets ahead of rising risks of renewed US sanctions pressure in early autumn following a six-month pause,” RenCap commented.

The government will welcome the key rate cut, but the CBR warned, as usual, that any deviation in 2026 budget parameters could prompt a review of monetary policy, citing risks from rising fiscal spending, oil price volatility, and geopolitics.

Federal budget discussions and drafting begin in August, with pressure mounting for cuts outside protected defence and security expenditures.

The analysts suggested by The Bell note that while the consecutive rate cuts mark a policy pivot aimed at softening the economic slowdown, the regulator is unlikely to abandon double-digit rates soon.

Russia thus continues to operate under a “high rates, slow growth” scenario, with monetary policy closely tied to fiscal developments in the coming months.