Bulgaria records EU’s sharpest fuel price rise in May

1 day ago

Turkish corporates’ credit quality weakened in 2025, leading to downgrades on four higher-rated companies, S&P Global Ratings said on December 1 in its Turkish corporate outlook for 2026.

The report (![]() S&P Turkish Corporate Outlook 2026.pdf)

S&P Turkish Corporate Outlook 2026.pdf)

Reasons behind the Turkish corporate downgrades executed in 2025 include a mix of ongoing economic challenges, alongside some company-specific factors, the rating agency said, adding: “There is limited further downward rating pressure going into 2026, with only one negative outlook among rated issuers.”

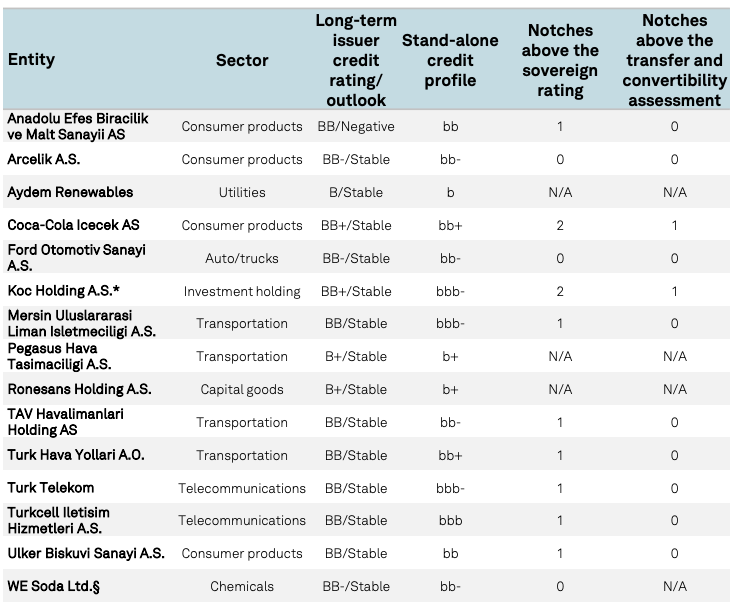

Table: The list of Turkish corporates rated by S&P.

Chart: 2026 risks by sectors.

Rate cuts to support leverage

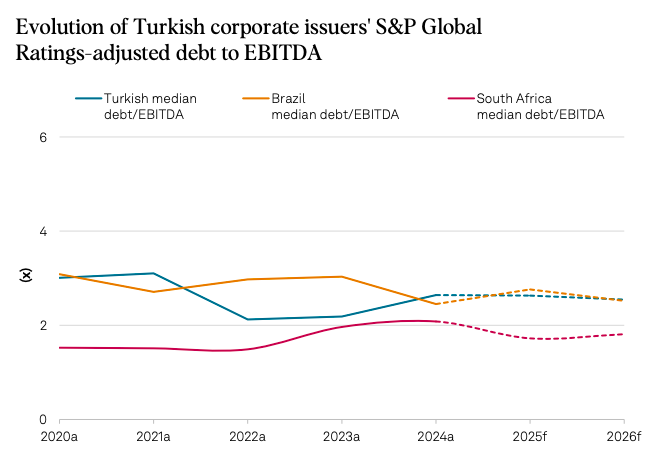

High interest rates continue to be the most significant credit factor for Turkish companies while the median leverage ratio (debt to Ebitda) remains healthy at 2.6x.

However, S&P forecasts improving trends in interest coverage and free cash flow based on a projected reduction in the headline policy rate.

The rating agency does not anticipate balance sheets will weaken further. It continues to expect healthy leverage metrics for Turkish corporates in 2026, in line with emerging market averages.

The increase in leverage from high inflation, weakened demand, high interest rates and exchange rate fluctuations, materialised in 2024 and should not intensify.

Turk Telekom (TTKOM) is the only company where S&P has recently revised its forecast such that leverage increases materially in 2026 due to concession payments and potential costs associated with the 5G spectrum auction. However, this does not relate to any performance aspects.

Chart: Debt to Ebitda for Turkish, South African and Brazilian corporates.

Weak domestic demand outweighs tariff woes

Weak demand and rising costs are stronger material risks for rated Turkish corporates than global trade factors, which are primarily impacting export industries such as steel and textiles.

S&P expects only a gradual recovery in domestic demand in 2026, even if the government achieves its inflation reduction targets.

Real lira appreciation hurting exporters

The significant real appreciation of the Turkish lira (TRY) versus the USD could hinder the exporters’ position. However, S&P thinks this hindrance could prove temporary.

Costs for export companies, historically more isolated from local conditions, have increased materially, in some cases affecting their global competitiveness.

Cost inflation has not been offset by a similar lira devaluation, as usually happens in emerging markets. Moreover, the stronger lira exacerbated the impact of high inflation.

S&P thinks costs should normalise in 2026, however.

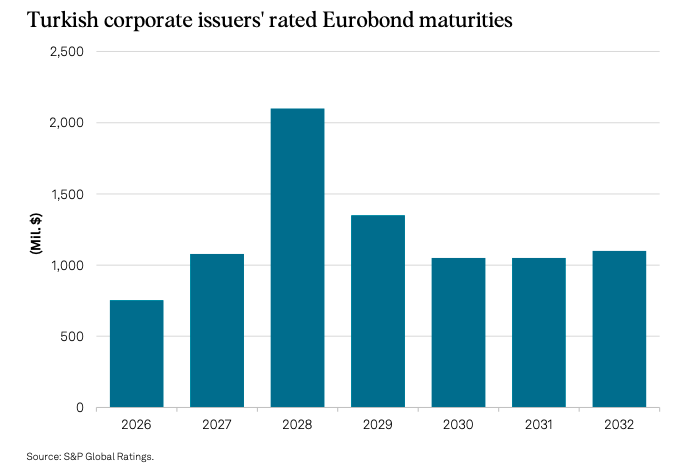

No rollover pressure by 2028

Liquidity profiles for most rated Turkish issuers are solid with no material overall refinancing needs until 2028, when the next peak of over $2bn in outstanding eurobonds is due.

S&P views this peak as manageable.

The eurobond market remains fully open to Turkish companies, lowering refinancing risk. Many corporates and banks have issued bonds recently.

Chart: Eurobond redemptions.

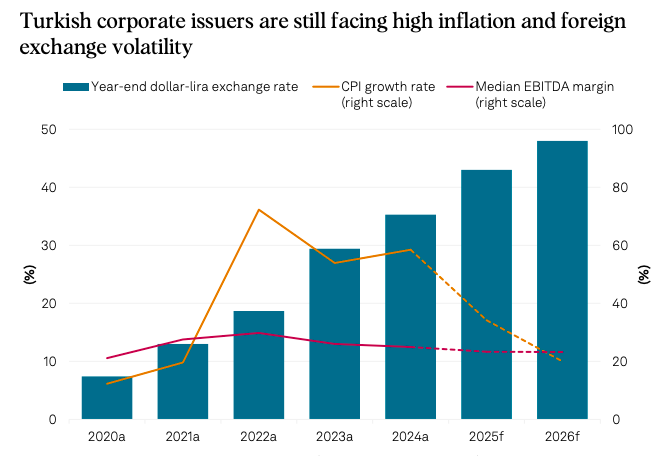

Resilient profitability despite hyperinflation

S&P expects rated corporate issuers to maintain resilient profitability despite the country’s economic challenges. Most Turkish issuers have absorbed inflation, maintaining resilient profitability.

Still, sectors like telecoms (Turkcell (TCELL) and TTKOM) fare much better than consumer goods (Anadolu Efes (AEFES), Arcelik (ARCLK), Coca Cola Icecek (CCOLA), Ulker (ULKER)), in which companies used steep promotional and discount efforts to drive volume at the expense of profits.

Chart: Turkey’s inflation, USD/TRY, EBITDA margins.

Telecoms (TTKOM, TCELL)

Turkey’s telecommunications sector is largely resilient to the economic cycle and inflation, given strong pass-through mechanisms. Capital investments in the industry are, meanwhile, high due to 5G development.

Interest rates could influence free cash flow and interest coverage metrics, according to S&P.

Airlines (Turkish Airlines (THYAO), Pegasus Airways (PGSUS), TAV (TAVHL))

The airlines sector is mostly driven by global factors with domestic developments having less of an impact. Margins could erode should inflation remain high and the lira appreciate further, S&P determined.

Consumer Goods (AEFES, ARCLK, CCOLA, ULKER)

Inflation and global trade conditions are key risk factors for the consumer goods sector. Heightened discounts and efforts to stimulate demand across durables and nondurables sectors have been employed since early 2025.

Interest rates could influence free cash flow and interest coverage metrics, according to S&P.

Infrastructure (Ronesans Holding, Aydem Yenilenebilir (AYDEM))

There is lower sensitivity to risks from unfavourable developments in the local economy and inflation for the infrastructure developers. Key investments in renewable energy projects flowing from government policies remain a tailwind for utilities (Aydem Yenilenebilir (AYDEM)).

Capital Goods (Ford Otosan (FROTO), Koc Holding (KCHOL), Mersin Liman)

High cyclicality exposes the capital goods sector to risks from domestic economy and global trade frictions. Persistent inflation could impair exporters’ competitiveness (Ford Otosan (FROTO)).

Interest rates could influence free cash flow and interest coverage metrics.

Exporters (We Soda, ARCLK, ULKER, AEFES, CCOLA, FROTO)

Global trade is the key risk factor for exporters. Direct impacts from the US tariffs are, meanwhile, limited. The lira’s appreciation threatens the global cost position.

For other export-oriented companies, indirect effects from global trade volatility are more pressing, said S&P.

The IntelliNews PRO service includes access to reports, exclusive market data, and more news that decision-makers care about. Stay ahead of the market with IntelliNews PRO.

Sign Up Now

_1_1781792042.png)